The Trade Desk: The High Growth Company Of The Future (Issue #15)

The Trade Desk: The High Growth Company Of The Future (Issue #15)

The Trade Desk

TTD: $49.78

Market Cap: $24.21 billion

Enterprise Value: $20.39 billion

Company Overview

Ad-supported streaming is the biggest trend in the business. And advertisers want their ads targeted to the right customers, this is where The Trade Desk comes in. In order for ads to be precisely targeted, they require demographic information. Unfortunately, this has led to multiple social media and tech companies like Google and Facebook gathering large databases with personal information. This has caused problems with the advertising space as access to the databases is a restricted walled garden. Advertisers now are looking for more transparency within the internet. The Trade Desk is at the forefront of this new movement–optimizing effective marketing online while also not having to gather deeply personal profiles on individuals.

Streaming creates value by increasing the number and value of users. For the value portion, this means higher ARPUs. In the case of non-ad services, this means higher subscription rates. However, with ad subsidized content it is possible to increase the ARPU by having more targeted ads. This is made possible by companies like The Trade Desk that are designed to increase ad effectiveness. And advertisers are willing to pay twice as much to The Trade Desk for TV advertising because of how effective it has proven to be compared to traditional TV advertisers.

The Trade Desk is a part of the Alternative Streaming Index because it works in ad distribution in streaming media (among other things). Ads are becoming increasingly important in streaming and the goal of the index was to follow companies that are involved in streaming in some way but are a degree of separation away from the big names like Disney and Netflix. The Trade Desk is a key part of building the future of streaming and the ads that accompany it.

The Trade Desk is an automatic programmatic marketing company founded in 2009. This means they work to distribute ads on podcasts, websites, and most importantly for our streaming services. Trade Desk operates as a Demand Side Platform (DSP) meaning its customers are marketing agencies who want the best return on their digital advertising investment. DSPs often work with Supply Side Platforms (SSP) like Magnite (also a part of the Alternative Streaming Index), SSPs work on the viewer side of online advertising and work to optimize results on that end. DSPs and SSPs working in tandem have shown to be very effective for marketing agencies.

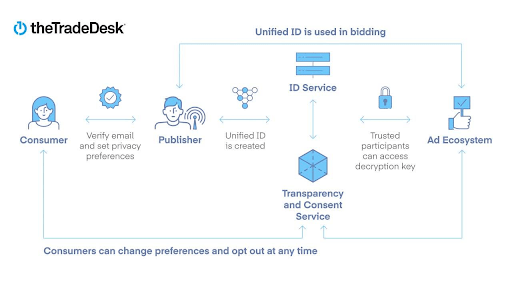

The Trade Desk uses an original Unique Identifier (UID) that replaces the Third Party Cookie (3PC). WIth cookies becoming obsolete and privacy becoming a bigger concern The Trade Desk has developed a way to anonymously link information to email addresses. This allows for the best parts of targeted online ads to be possible while also not participating in personal data collection. This seemingly small, but important difference is the thing that sets them apart from companies Google and Facebook/Meta and allows them to compete with these giants.

In Q1 2022 conference call, Jeff Green commented on UID:

The Internet has been operating on a quid pro quo since it became commercial, but the Internet has been a suboptimal Internet. And by that, I mean we've used cookies as a make-shift technology to enable relevant advertising. But due to a series of events and choices, cookies are going away. Currently, Google has the majority of the browser market share around the entire Internet outside of China. So they decided when this transition is going to take place, and they currently targeted the end of Q1 2023. This has created a very unique community to upgrade the Internet. Indeed, without those many circumstances, this opportunity wouldn't exist. We are upgrading from an opt-out Internet to an opt-in Internet.

The open Internet is scrambling to coordinate and collectively upgrade. Many different opt-in IDs are being created. Some of them will scale and survive, some won't. However, those that scale will be distributed, encrypted and interoperable. We don't believe IDs can or will scale if they don't upgrade the experience for consumers.

With this in mind, we developed and launched UID2.

The Trade Desk is run by its founder Jeff Green who also founded a demand-side advertising platform that was acquired by Microsoft in 2007. Management is veterans in the space and has proven they can punch above their weight. The UID is also an improvement because it works on Smart TV and Mobile, a key component the cookie was lacking. This also allows more opportunities to gather anonymous data. Advertising agency customers have more distribution opportunities and more data increases the accuracy of the ads.

Diagram Showing UID Use-Cases

The interactions use UID as the exchange between marketing agencies, DSPs, and SSPs are online auctions that occur within seconds, are completely programmatic, and powered by data.

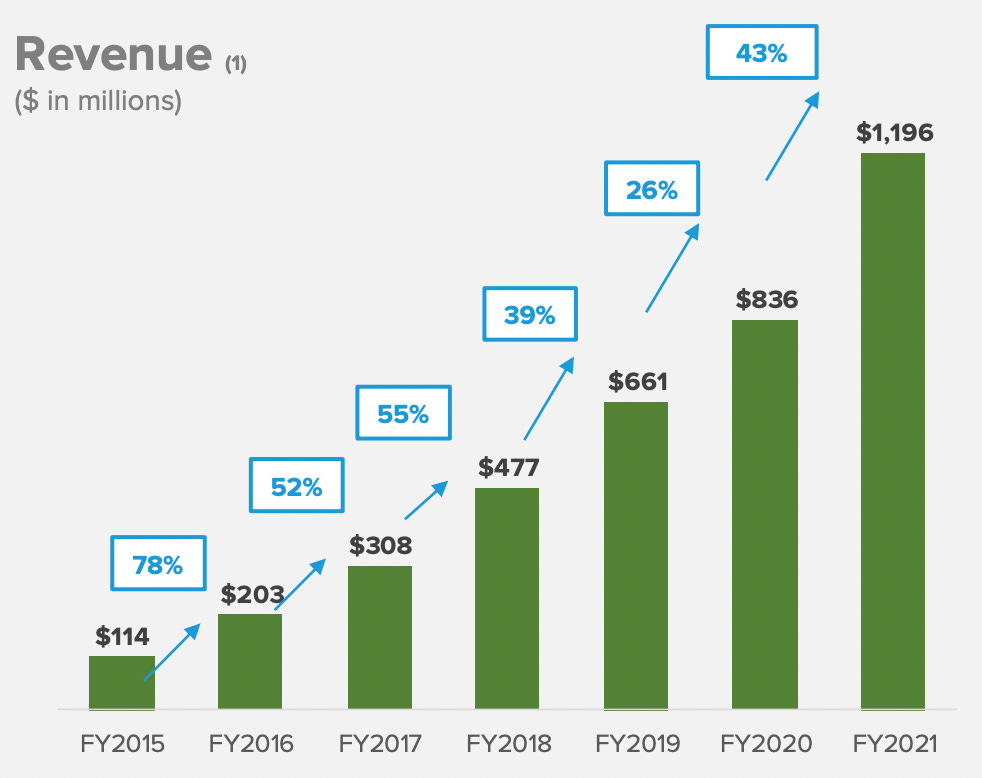

Revenue (as shown below) has been growing on average ~47% annually since 2015. Growth year/year has only increased from an already high rate. Because The Trade Desk is directly connected to streaming and tech companies it was more hard hit recently compared to other companies. This was part of the equal and opposite reaction from companies that were advantaged by the pandemic now hurting. However, The Trade Desk is only becoming more in demand as companies like Netflix and Disney look for ways to increase revenue as the once avid users begin to return to their old normal that allotted for less time at home.

The Trade Desk Revenue Growth By Year, Source: The Trade Desk Q1 2022 Earnings Report

Revenue is growing. Margins are growing. And on top of all that FCF is growing too. FCF even doubled year/year for the company. This is important because this shows that the business is not killing itself to grow and instead becoming a better business as it grows.

Business Outlook

Streaming is an important territory for The Trade Desk because connecting advertisers to omnichannel distribution set them apart. This is why in these early stages of this part of the streaming wars partnerships between marketing companies like Trade Desk and streaming companies are so valuable.

The graphic above not only includes multiple important players in the Alternative Streaming Index, but also many important players in the greater streaming industry like Viacom/Paramount, ESPN (Disney), NBC (Peacock), Roku TV, and more.

Even the streaming companies that have tried to be known for quality by not having ads–Netflix and Disney+–are being forced to incorporate ads to support their business. Content is king, but it is also costly and as the streaming wars become bloody more capital is necessary to succeed. This means using well-targeted ads that achieve high CPMs to afford the best and/or most content. The Trade Desk’s UID has proven its ability to bring in those higher CPMs.

The Trade Desk already has a significant market share outside of North America. However, in North America, the company accounts for a third of all advertising spending. This is significant, but there is still a lot of room to grow, and as the company mentions the space is still growing. There is an estimated almost $1 trillion TAM for the advertising market showing that there is plenty of room for the company to grow into.

One thing that really sets The Trade Desk apart from its competitors in omnichannel. This allows The Trade Desk to advertise to viewers on multiple different platforms/mediums. In addition, The Trade Desk can also retrieve more insight into viewers’ preferences because they have more platforms worth of data collection.

The Trade Desk derives most of its revenue from North America, but advertisers are increasingly global with more ad revenue spent outside the US. From 2015 to 2021, The Trade Desk grew its non-North American revenue from 6.5% of revenue to 14% of revenue. There is more growth to come overseas.

The Trade Desk operates as a demand-side platform meaning it gives the advertiser control. This is important for acquiring clients like Walmart and this is a major differentiator from Google and Facebook which are supply-side platforms and give the distribution platform (themselves) the power.

In my Peloton deep dive, I talked about how growth companies have to evolve to have strong balance sheets and cash flow statements. The Trade Desk is already there. On top of the high revenue growth, the company has more than doubled FCF in Q1 2022 to ~$137 million compared to Q1 2022 at ~$60 million.

Like in all businesses there are risks. Although The Trade Desk is designed to maximize anonymity privacy of viewers is an everlasting concern in the space. Connected to this companies like Apple through iOS have implemented anti-tracking software. This has hit Facebook/Meta’s sales hard but has yet to affect The Trade Desk. However, more implementations like this in the future could pose a threat to the company. Another important risk to note is that The Trade Desk doesn’t “have” any of these users only the platforms it partners with possess them. This means they could lose large viewership if certain partners pulled out.

Insider Ownership

There haven’t been many moves by insiders either selling or buying, but this year the inconsequential (in my opinion) trades have been larger buys than sells. However, I don’t think this is a strong indicator of anything.

Valuation

The Trade Desk is no value stock. The Price/Cash Flow is 51x however this is a tech company and high multiples aren’t uncommon in the space. This is also below the nosebleed 5-year average of 108x. Also, there aren’t many companies out there growing revenue at a high rate and having extremely high margins.

Growth companies are judged in part by the Rule of 40: A company's revenue growth rate plus its profitability margin should be greater than 40%

The Trade Desk has a year/year revenue growth rate of ~44% and a gross profit margin of ~82% making a total of ~126% meaning it easily passes this test. This is the kind of growth company that can survive in the new economic climate because it has the cores of a quality business. Not only is The Trade Desk growing it is growing quickly with an extremely high gross margin.

Until Next Time,

Soren