The Home Depot: Not Competing With Lowe's (Issue #42)

The Home Depot: Not Competing With Lowe's (Issue #42)

The Home Depot is more than the “do it yourself” (DIY) home improvement shop most think of. There are two main parts to the business, the consumer side and the pro side. Most of us are familiar with the consumer business because we’ve witnessed it firsthand. This business is very similar and often compared to Lowe’s. However, Home Depot only competes with Lowe’s in some parts of the consumer area; Home Depot sets itself apart from the rest of its competition by focusing on the hands-on DIYer and construction pros. Simply put, basically every time you see a pickup truck with a name on the side, they are in the Home Depot sweet spot.

Company Overview

Home Depot is a growth machine and an investor’s dream. The company grows in 2 ways. The traditional method is same-store comparable sales (comps) gaining more profits from existing stores. Home Depot has historically grown through both store count and comps methods very successfully. For example, in 2021 comps growth alone was 11.4% for the year.

The key differentiator of Home Depot between its consumer-focused competitors like

Lowe’s is their focus on the many construction and industrial suppliers. Home Depot can beat those suppliers not because of their prices, but because of their guarantee, they can have the part, tool, or material before you even get to the store. And the stores are located close to where their customers need them. This is helpful for consumers, but crucial for contractors, plumbers, electricians, etc who have a client who needs a job to be done as soon as possible.

Home Depot has grown substantially until now, but how much more room is there to go? They estimate their TAM at ~$900bn–half of this revenue from the consumer business and half from pro-business–this is four times their current revenue and the company is currently being traded below a typical multiple (more on this in valuation).

You can’t talk about Home Depot without mentioning their astronomically high Return On Equity (ROE) which currently sits at ~1,466% TTM and peaked at ~14,061% in 2021. However, it is important to compare this to the Return On Invested Capital (ROIC) which rests at a still very respectable ~37% TTM and ~34% in 2021. The massive difference between ROE and ROIC is due to Home Depot’s debt which they leverage for more growth as well as their formidable 2.38% Dividend Yield. In spite of both of these factors, Home Depot has been able to overall become more efficient with their return. This can be seen in the increase in ROIC and decrease in ROE.

Looking Forward

Home Depot has come a long way from where it once was, a single store in Atlanta, but there is still a lot of room to grow and value to be created from it.

It is hard to talk about almost any business without talking about how Amazon might beat them out of their own industry. Home Depot has a huge defense against the behemoth, ~2,300 physical stores that average 104,000 sqft and an additional 24,000 sqft for gardening supplies. That is not infrastructure that can be quickly, cheaply, or easily duplicated. Further, it is difficult and expensive to ship wood, tools, construction materials, or the many other heavy objects Home Depot sells. Finally, as all of us who have done some of our own home improvement know, not all wood is created equal. Therefore, all the consumers and pros who are buying it, want to see the product in person before purchasing it.

A separate, but equally important moat is Home Depot’s commitment to their customers and providing the best service. When I have talked to many consumers there is an even split between those who like Lowe’s vs. Home Depot. However, when you research statistics on how pros feel about Home Depot it is shown that they would drive an additional 6 miles to go to a Home Depot over a competitor. This is a product of the systems that have been put in place by the company to ensure the best service possible. These are things like an app to easily and quickly guide pros to the exact shelf of the product they are looking for or curbside pick up so they don’t even need to leave the parking lot to get everything they need for a job. This means their moat here is in efficiency to the customer, especially pros. No other retailer or construction supplier not even Lowe’s offers essentially “in-store google maps” within the store to find the product you are looking for or will bring it out to your car so you don’t even have to go in the store. Home Depot understands that this is not about your DIY home improvement project it’s about the one-person carpentry or plumbing or electrical business that needs to have a reliable and fast supplier. Home Depot has shaped its company to serve this purpose. This connection with their customers based on better service, both faster and higher quality means they can charge more than competitors and still be preferred by their markets.

The dividend and the revenue growth are important, but buybacks also have driven value for investors over the years. Over the last 5 years, Home Depot has averaged ~3% buyback yield to investors. This combined with the continually strong dividend makes a real value driver for investors.

One of the first concerns that comes to mind with Home Depot looking forward is an inevitable slowing in new homes being built. However, people continually and regularly remodel or alter their homes which Home Depot serves as well. Further, a third of their current pro revenue comes from Maintence, Repair, and Operations (MRO). This is a business that is not going anywhere anytime soon.

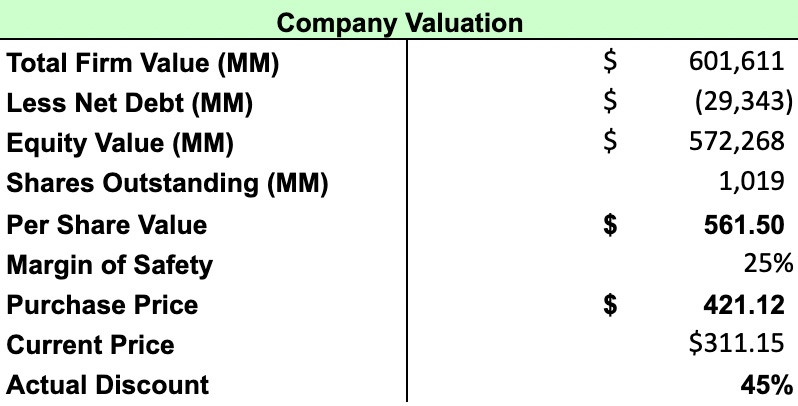

Valuation

Home Depot has grown Free Cash Flow (FCF) alone by ~17% annually over the past 5 years without increasing the store count. In the DCF I used that would be used as the value growth metric, but I reduced it down to 12% to be more conservative. While the discount from fair value is not a massive discrepancy it should also be realized that Home Depot as will other companies does not simply stagnate after this projection and has the ability to keep growing. The company projects its TAM revenue to be almost four times its current. There is plenty of room for this company to grow over the long term.

Aside from the DCF Home Depot currently trades at some very reasonable multiples. For example, a ~19x Price/Earnings and a ~24x Price/Cash Flow. These may not be value investor numbers, but they are low for what is often considered a growth company.

Investment Thesis

Home Depot is the latest holding in the Pillars and Profits Portfolio. It is a clear choice when you see the powerful long-term growth potential combined with strong moats and multiple other value-creation avenues with dividends and buybacks. Although it is not clear on the surface Home Depot has created its own niche and won the market niche it created.

Until After The Holidays,

Soren

Disclaimer: Soren Peterson and Pillars And Profits Newsletter are not responsible for any investment results. This is not financial advice. Always do your own research.