Sunday Updates: Is Magnite Better Than The Trade Desk? (Issue #18)

Sunday Updates: Is Magnite Better Than The Trade Desk? (Issue #18)

Big announcement! The Streaming Jungle is ending. This newsletter is being converted to Pillars And Profits, a newsletter that tracks a “single digit portfolio” . It will focus on the companies I personally own or am seriously considering. Alternate Streaming coverage will continue on another platform, Media Bytes! This is the last formal Sunday Update via Streaming Jungle but will do Monthly Updates and Quarterly deep dives on Media Bytes.

Your current subscription will remain here (subscribe if you haven't already) and subscribe to Media Bytes for future streaming content.

The posting schedule for the newsletter will remain the same, but this is the last strictly streaming post. Tune in next week to hear the first 3 companies in the portfolio.

Magnite Inc

MGNI: $8.55

Market Cap: $1.13 billion

Enterprise Value: $1.78 billion

Company Overview

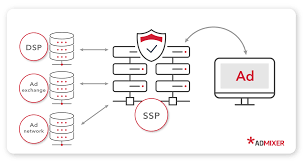

Magnite is a supply-side platform (SSP) in the online and media advertising space. SSPs sit across the table from demand-side platform buyers (DSP) like The Trade Desk. This space can often seem confusing when differentiating between SSP and DSP. Don’t they do the same thing? Not quite. DSPs work with ad agencies to maximize the number of impressions for the least amount of money. This is about optimizing effectiveness and making each impression count for as little as possible. SSPs do the opposite. They partner with “publishers” (the displaying platforms) to maximize how much they get paid for impressions. Often the two work together and have virtual fully computer-operated auctions. If you missed the write-up on The Trade Desk check it out here.

Both Magnite and The Trade Desk are important to the growth and success of advertising in streaming. They both benefit from the sector as a whole growing. The growth stems from the novelty of ad tech and also ads becoming increasingly important parts of streaming. For example, Warner Brothers Discovery just announced it is launching a fully ad-supported tier. Even Netflix as well as every other major streamer is incorporating ads into its service. However not all ad-tech is created equal, as we dive in further it will become clear that the DSP seems to be a better business than the SSP. Both have comparable growth, but The Trade Desk has far higher margins and ROIC.

Magnite itself was built on a merger of Telaria and Rubicon Project. These two companies combined in April 2020. The merger gave Telaria shareholders ~47% of stock and Rubicon Project shareholders ~53% of the stock in the new company (Magnite).

Source: AdMixer

Diagram of the collaboration/roles of DSPs versus SSPs. However, DSPs can go direct to the publishers (the displaying platforms) and get rid of the SSP. It isn’t really possible for SSPs to do the same.

Business Outlook

Although Magnite gets paid by the advertising agencies or DSPs, it works on behalf of the publisher or display platform. Magnite makes deals on computer operated auctions with Google Ads or The Trade Desk. These negotiations use CPMs as well as many other measures of user engagement and applicability to a product to find the right price for each deal.

The ad-tech industry is still in its early stages and it is growing quickly. It is becoming increasingly important to the effectiveness of advertising while maintaining anonymity online. This is supported by their numbers. Revenue as a whole grew by 79% in Q1 2022 year over year (Y/Y) to $107.1 million. Importantly, looking at the company from a streaming perspective CTV (Connected TV) revenue grew by 253% Y/Y to $42.3 million in Q1 2022. Streaming and TV is a clearly significant portion of the business.

Earnings Per Share (EPS) grew Y/Y from $0.03 in Q1 2021 to $0.08 in Q1 2022. On top of this Cash from Operations was $21.6 million in Q1 2022 from -$1.2 million in Q1 2021. In the Q1 2022 earnings report, Magnite basically kept in line with expectations. They slightly beat expectations, but overall we’re not meaningfully above their projections and did not raise their future goals. This does not inspire confidence in investors as this is a high-growth space and beating and raising is par for the course when over 50% revenue growth, high free cash flow, and large margins are standard.

Growth by Acquisition

Magnite is always a fan of a good acquisition. This has been a trend in the ad-tech space in general, but Magnite accentuates this trend. For example, they purchased SpotX for $1.17 billion in April 2021. The company capitalized on the additional shareholder funding of the time (Market Cap of ~$5.2 billion at time of acquisition) to make this sizable purchase. The smaller acquisitions are done with cash, but the big ones like SpotX are a mix of cash, debt, and equity. With a significant majority of debt and equity. The split is ~$200 million in cash, ~$500 million in debt, and ~$500 million in equity.

These acquisitions are important because Magnite values Goodwill at almost $1 billion on its balance sheet. This is seemingly accurate based on the sheer amount of acquisitions, but I am often wary of intangible assets and ways value is “created,” for example, Goodwill and Accounts Receivable.

Valuation

Magnite trades at 8.38x Price/Cash Flow. This is extremely cheap especially compared to The Trade Desk at 55x Price/Cash Flow. There is a discount for a reason. The space as a whole can be leapfrogged with some strategic moves from DSPs. Technically speaking SSPs can do this too, but it is only advantageous for the publisher whereas DSPs going direct can be advantageous for both the publisher and the advertiser. On top of this DSPs have ultra-high margins and ROIC especially in comparison to SSPs. Both have high revenue growth, but beyond that DSPs seem like a much better option.

Until Next Week,

Soren

PUBM > MGNI