Schools, Churches, and Banks: Takeaways From The Banking Symposium #2 (Issue #91)

Schools, Churches, and Banks: Takeaways From The Banking Symposium #2 (Issue #91)

I had the opportunity to attend and be a part of John Maxfield’s Banking Symposium in Dallas. The Banking Symposium is a gathering of many of the top bankers in the US. It may sound like a conference but don’t be deceived. It is hard to put into words the full value of the event and the form of how it took place, so here is my best attempt at some of the highlights and takeaways.

Maxfield led off with an example of why banks are so important to towns and cities. They are a pillar of the community. There are three cores of every town: schools, churches, and banks. All of these facilities are both supported by the community and give back to it. It’s an ecosystem. What great bankers understand better than anyone else is that if you feed the community the community will feed you. This is why great bankers emphasize community outreach and initiatives to give back. For example, during the symposium, we had the opportunity to visit the Triumph Workshop. The Triumph Workshop is a branch of Triumph Financial focused on helping members of the community learn key technical skills to build careers in the trades. They notably didn’t just throw money at a problem and instead created a system for positive change.

One of the recurring lessons during the symposium was “abundance begets failure.” This is of course in reference to some of the bank failures from 2023. Namely Silicon Valley Bank and Signature Bank. These banks saw a rapid increase in their deposits without a competent investment strategy for the large influx of capital. The company decided to buy fixed-rate long-term government bonds which gave the portfolio an average return of 1.79%. This gave the bank no margin to operate with when trying to run operations, pay interest to depositors, etc. This connected to a later point made by Mark Lynch formerly of Wellington: No change is bad as customers widdle away margins, fast growth is bad (as seen here), but slow and consistent growth is the only way to win in banking. By remaining surefooted while constantly working to incrementally improve banks can succeed over time. Investors look for growth banks and never learn (i.e. First Republic, another victim of 2023).

Success in banking is not created by over-extending yourself in boom times and instead holding back while others are being gluttonous. This allows for less risk in the bust times. This goes back to the ideas of consistent and incremental growth and improvement over time. Large shifts in bank performance through market cycles do not bode well for the company’s success.

“To be fearful when others are greedy and to be greedy only when others are fearful.”

- Warren Buffett

Similarly to investing opposing or different strategies can both work. For example, Ross McKnight, who built Interbank into what it is today, refused to invest in stocks or bonds both within his bank and personally. McKnight has seen great success throughout his time building his banking empire with this constraint. However, there have been many examples of successful banks that use a stock or bond portfolio as a leverage point for growth. On a smaller scale, Hingham Institution For Savings has successfully began to use its investment portfolio to grow. This demonstrates the importance of playing to your own strengths as a banker and business person.

This clearly connects to another idea raised at the event of growth through compounding book value and doing so without being levered to one thing. Otherwise, you end up with an over-concentration or dependence on one thing. This can make you especially vulnerable to sudden or drastic changes in that area. In this newsletter, lack of diversification is an idea I talk about a lot. Why would you dilute something good with something worse, in your portfolio, in some misinformed pursuit to be “safer.” However, banks operate in such a crucial place within our communities and economies that they have to be fortified against recession and crisis. They must have many strong pillars that hold them in place.

The final concept from the event I’ll mention is: density wins. Community banks are not at risk of being wiped out by big (or larger) banks, at least not all of them. Density within a market is a massive competitive advantage. Local community banks often have the saturation that a big bank entering a new market would never work to achieve. There’s no logical reason why Bank of America or another big bank would put more than one branch in Hingham, MA; Auburn, AL; or Zachary, LA. However, Hingham Institution For Savings, AuburnBank, and Bank of Zachary all have multiple branches in their respective hubs. While each of these banks operates very differently and are even quite different in size they all have a hub in a small city or town with a unique coverage of that market. It is difficult and not a fruitful pursuit for most other banks to attempt to take over that area. A single branch from another bank could do well in Hingham, Auburn, or Zachary, however, local bank’s moat would only marginally be eroded. That being said, the moat only goes so far. It is only the best-run and most dense banks that will survive crises with this kind of competitive advantage. No town or small city can give 3, 4, or even 5 local banks a local moat, but 1 or 2 can well-operated banks can benefit from being a key player within a market. Additionally, at a certain scale of the market (i.e. bigger cities) the moat is weaker or non-existent.

The Banking Symposium cannot be contracted into a list of takeaways or any newsletter. It is an amazing event and I cannot recommend it enough. Subscribe to stay tuned for updates and information about these events.

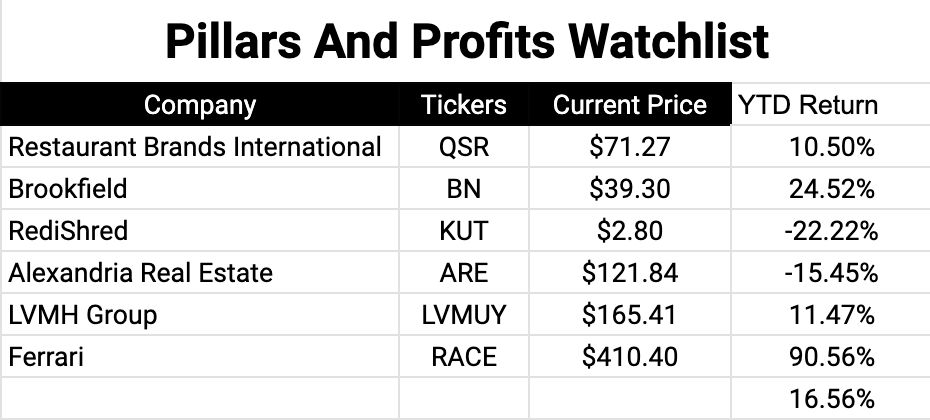

Watchlist Update:

Portfolio Update:

Until Sunday,

Soren

Soren -- Great write-up. Sad I could not make the event this year but share your enthusiasm for it as the Philadelphia symposium far exceeded my expectations. Building on your incremental growth comments, I have a 23-year relationship with a community bank that has consistently produced a 90th percentile ROA using that same approach. They average 7-8% asset and earnings growth with a low standard deviation. The most "boring" group of bankers producing the most "exciting" returns!