Redi Or Not: RediShred The Dominant Underdog (Issue #39)

Redi Or Not: RediShred The Dominant Underdog (Issue #39)

RediShred Capital Corp.

Ticker: KUT.V $2.90

Market Cap: $71.52m

Enterprise Value: $93.38m

Company Overview

Background

RediShred is the company that holds most notably PROSHRED, a paper shredding franchise business for small to medium-sized enterprises (SME) as well as doing some electronics disposal. RediShred is managed in Canada but operates almost entirely in the US. PROSHRED operates in 21 different states and 40 different markets. RediShred has been around since 2006. It began when PROSHRED started in the Philadelphia market.

The paper shredding and disposal industry is a $3.6b market where RediShred is the distant third-largest by market share. The largest player is Iron Mountain with a 25% market share, however, they focus on working with large companies. Next is Shred It which is owned by Stericycle as of 2015 and controls a 20% market share. This is the main competitor to worry about because Shred It has mainly focused on SMEs similar to PROSHRED. PROSHRED holds a little over 1% market share. The next 30% of the market share is accounted for by independent operators who almost universally have 2 trucks or less and less than $500k in revenue annually. Finally, the last 25% use in-house shredding facilities.

The biggest differences between the services include Iron Mountain and Stericycle offering other services like other types of specialized waste management for mainly medical products. For paper shredding specifically, the companies are very similar in their services with trucks coming to pick up to be shredded paper. In some cases, the companies shred on-site.

Paper and physical documents are increasingly being viewed negatively by investors. This has caused an exodus especially when many speculated on paper becoming obsolete during and after the pandemic. However, paper usage for the purposes that need to be shredded is actually steadily increasing over time and the returns of companies in the sector reflect this to be true. These include industries like medical, legal, and financial management/services. There were hits to the industry on a short-term level in Q1 and Q4 of 2020, but…

the sector has since fully rebounded. However, the stock of RediShred still trades below 2019 levels despite having high revenue and earnings.

Shredding itself is the core of these businesses, but another key is the sorted office paper (SOP) selling business. This is when PROSHRED or any of its competitors shred paper and recycle it to make more paper. This is Charlie Munger’s idea of selling oil, putting it back in the ground, and selling it again in action. These businesses get paid on both ends of this system. They first get paid to collect and shred the paper and get paid again when they resell the recycled paper. This means that SOP sales are almost pure profit. It is important to note that the price of SOP can be volatile and that this has affected PROSHRED’s earnings most notably in 2020 when SOP prices dropped to $67 per ton from its peak of $185 per ton in 2018. Over the past 10 years, the average price has been $135 per ton and the price is now hovering in the $150 per ton neighborhood after spiking to the $175-180 range in May 2021.

Reusing/recycling paper has many positive Socially Responsible impacts too. For example, in 2021 RediShred saved 778 thousand trees averaging ~193 thousand a quarter from being cut down by reusing the shredded paper.

RediShred has been a strong returning business for a number of years because of a combination of multiple important tactics. First, they try to start new franchises to expand their footprint and personally assume little risk in testing new markets. Next, they work to repurchase franchises from franchisees in proven markets to assume more value from them. RediShred has paid up to 5-6.5x EBITDA for proven franchises. RediShred will also buy out its smaller competitors, however, these will be at lower multiples. On the high end 4x EBITDA, but sometimes as low as simply the worth of the trucks. This depends on if the acquisition is happening in a market that RediShred is already dominant in or a market they want to expand to.

RediShred spent $16.6m on acquisitions of 4 shredding companies in 2021 across 4 states. This is a 4% increase from 2020. There are some signs of slowing with only ~$2.3m in acquisitions split between the acquisition of 2 companies in the first half of this year, but they do continue.

RediShred had a revenue CAGR of 30% for the 6 years before the pandemic with the lowest revenue growth rate of 23% in that period. It is important to note here that a significant portion of these returns were due to conversions between USD and CAD (RediShred is managed in Canada while it operates in the US) and the maximization of selling SOP at high prices. Although management did use these devices to its advantage it could pose a threat to the future with the uncertainty of currency conversion rates and SOP prices. The difference in returns is shown most drastically when looking at the company-owned branches’ revenue same-store sales in USD. This produces just a 9% CAGR and a minimum revenue growth rate of 5% in 6 years before the pandemic. All of these growth rates are only looking at organic growth and therefore do not include growth caused by acquisition which adds to the growth of RediShred. Looking at all growth both organic and not revenue has had a median growth rate of 33.9% over the past 5 years (not pre-pandemic, just 5 years from 2022).

Business Outlook

The outlook for RediShred is positive because of the moats in place to protect the PROSHRED business and the strategy it is executing to increase returns and scale. The moats include barriers to entry and the existence of smaller competitors like route density, marketing strategies, and perceived amount of sophistication for important work like this. PROSHRED is a large enough company to have enough customers to maximize efficiency with route planning and density. On top of this PROSHRED also can devote some energy to marketing and creating strong networks before competitors. Finally being a larger company PROSHRED has the perceived value and sophistication to be chosen over a local “a few guys and a truck” operation.

There is some secular growth, but most growth stems from acquiring franchises and small mom-and-pop-sized competitors. These smaller M&A transactions are very similar to the ones we see in HVAC companies trying to gain market share. Because of lower-than-average shredding recently caused by the pandemic sorted office paper (SOP) rates have rocketed up to $150 per ton. The paper shredding has since recovered from the lows of Q1 and Q4 of 2020. However, the market has still looked poorly on RediShred in spite of recovering returns and reaping the rewards of the increased SOP prices.

Management while continuing to grow comparable same-store sales by beating out smaller local players also is growing its footprint through acquisitions of smaller competitors and the repurchasing of franchises from franchisees. By expanding this way RediShred takes on much less risk because they can choose to buy already proven and working operations or less functional ones at a discount.

Management plans on continuing this strategy for growth and because of the market share distribution this is a sustainable tactic.

Insider Ownership

In total, ~12% of shares are held by management. The highest stakeholders are Robert Kay a member of the board and Robert Crozier board member and former CEO of RediShred (2009-2011)

Almost all board members just purchased more shares at the end of April of this year. This is as they have continued to be looked at unfavorably by investors even though revenues and earnings have fully recovered to pre-pandemic levels.

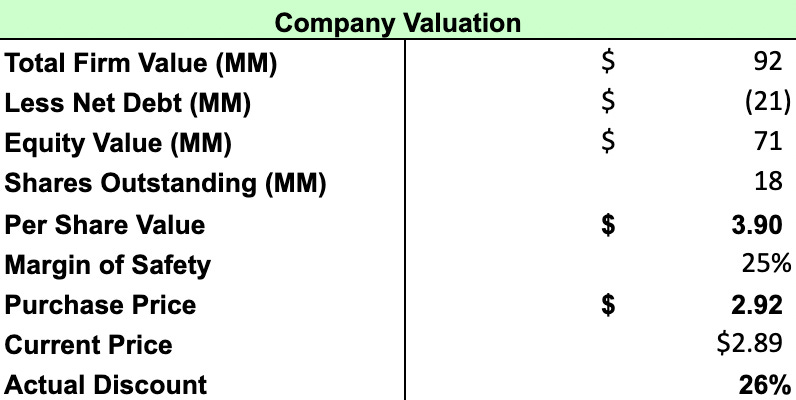

Valuation

The stock does look undervalued. Using a basic discounted cash flow model (DCF) the fair value of the shares is $3.90 USD while they are currently trading at $2.89 USD. This is more than clears the 25% margin of safety I used as my guide for how good of a buy RediShred seemed based on valuation. I have included a link to my DCF here. Below includes some of the outputs from the DCF. In the past 6 months, RediShred has gone through a reverse merger where they went from 91 million outstanding shares to 18 million with each share being worth more.

From another standpoint, RediShred is valued at a very high 95x Price/Earnings. This is made less extreme when looking at Price/Forward Earnings which is 30x or looking at Price/Cash Flow which is 7.5x. Cash flow is more of an important insight into the company because the high P/E ratio is partially a product of high acquisition costs from reacquiring franchises and competitors. This is why the company still seems undervalued and that idea is only supported by the DCF and P/C.

It is hard to see a catalyst for investors to once again have faith in the business. This may be a product of investors looking at a few years of strong returns because all other possibilities seem to be in action. These are things like insider buying, strong pandemic recovery, and sustained competitive advantages through adversity. For these reasons it is not in the Pillars And Profits Portfolio…yet.

Until Sunday,

Soren

Disclaimer: Soren Peterson and Pillars And Profits Newsletter are not responsible for any investment results. This is not financial advice. Always do your own research.