Preparing For HIFS Annual Meeting (Issue #58)

Preparing For HIFS Annual Meeting (Issue #58)

In preparation for the Hingham Institution For Savings (NASDAQ: HIFS — $395.51m) annual meeting this week I compiled some takeaways from their annual report.

These past couple of years have been extraordinary for the bank. This has been acknowledged and seen as an outlier by the CEO and COO, Robert and Patrick Gaughen (respectively). This past year was less of a blow-the-doors-off fantastic year. Instead, Hingham along with their competitors felt the effects of net interest margin (NIM) compression. Now with the addition of the still recent SVB events the 2023 fiscal year will also most likely be a challenging one for all banks including Hingham. In this years letter the managers have already acknowledged this weak point and foresee another difficult year. That being said a ~14%* ROE in a difficult year for a bank is not too shabby.

Now that Hingham is established in San Francisco and DC I will be curious to see how they continue to grow after the initial expansion, especially in these more difficult times.

Hingham has performed well for over a decade and I don’t see that changing anytime soon. The company culture management has created is impeccable and it is the corner stone of Hingham’s success so far. Their culture also allows them to withstand tough times.

For my full analysis on Hingham (HIFS) go here.

Questions for the meeting. If you have questions for the annual meeting this Thursday either join on Zoom, reach out to Patrick, or contact me (reply to this email or email pillarsandprofits@gmail.com). I’m curious to hear how they plan to mitigate effects of NIM Compression and what sets them apart in weathering that storm.

* ROE for last year was ~14%, however, it comes to 10% because equity losses when reporting. These losses are unrealized and therefore not included as part of the stat I like to use.

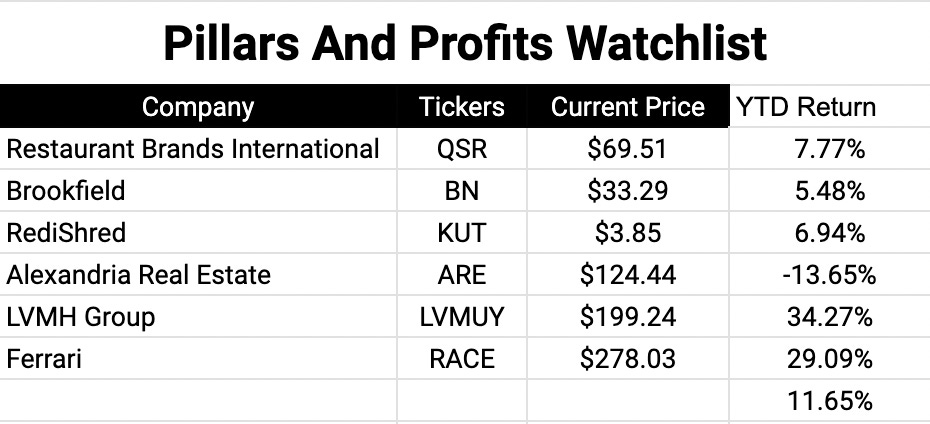

Watchlist Update:

Portfolio Update:

To see the full spreadsheet and linked deep dives go here.

Until Thursday,

Soren