Peloton Didn't Wake Up To Quit (Issue #9)

Peloton Didn't Wake Up To Quit (Issue #9)

Peloton Interactive

PTON: $9.82

Market Cap: $3.31bn

Enterprise Value: $3.99bn

Company Overview

Peloton was the poster child of growth of the past couple years and is the poster child again for the fall of companies advantaged by the pandemic.

Peloton is a “SaaS plus a box” company because although the box is a sleek stationary bike and treadmill, the real business behind Peloton is the technology and content that supports the physical products. Customers may spend anywhere from $1,200-$3,000 on a bike or treadmill and kit. However, to use any of their products you need to subscribe to their all-access service which is a $44/month subscription. So this model is closer to an AT&T or Verizon model from one perspective. Or from a streaming perspective an AppleTV and AppleTV+ or Amazon Fire Stick and Amazon Prime Video style model. In their earnings Peloton splits its revenue into two categories, Connected Fitness Revenue – revenue from bike and treadmill sales – and Subscription Revenue – revenue from their subscription for workouts, scenic rides, and runs.

Since Peloton is at the confluence of two markets it is hard to judge whether it will succumb to secular growth from the streaming industry. On one hand, Peloton has been a “Covid company” that has benefitted by increased hours spent at home. These types of companies have been recently hit hard as “normal” (whatever that word means anymore) resumes in a lot of senses once again. On the other hand, Peloton is long-tail streaming business which is why I put it in the Streaming Jungle’s Alternative Streaming Index. Peloton would like investors to think of it as a software and streaming company:

“What differentiates us is the software, which includes the streaming and the gamification and the network. We’re also a media company on top of that because we’re streaming 12 hours of live TV content each day and have another 4,000 classes on-demand.” – John Foley, CEO/Co-Founder Peloton

Needless to say, Peloton would like investors to value it as a tech company rather than a fitness gadget maker to garner a higher valuation. The question for investors is – which is it really?

Returns

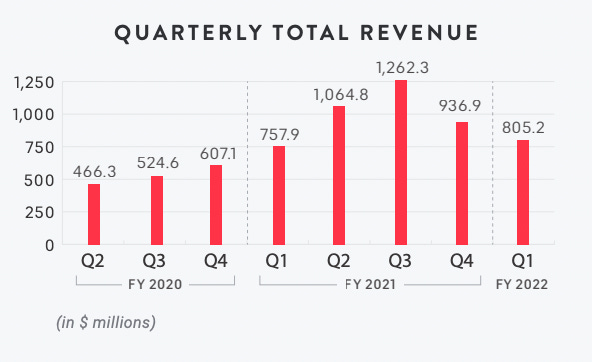

In Q1 2022 earnings there were some positives and negatives. Starting with some of the negatives Peloton has been feeling the effects of the core advantages they gained over the pandemic falling away. Although, workouts are up in Q4 and Q1 year over year, they are down from Q3 to Q4 and again from Q4 to Q1.

Source: Peloton Q1 2022 Earnings Report

Further, as people return to gyms fewer people are inclined to buy a Peloton or a subscription. This has been an important factor in the stock getting pummeled. This was foreseen by management but was disappointing nevertheless. Even the predicted lower revenue of $810m for the quarter fell short at $805m. Meanwhile, Connected Fitness Revenue is down 17% from Q1 2021, and marketing costs are up 148% to $284m for the quarter. This would be one thing if it were a slow grower missing its market, but Peloton is designed to “beat and raise.” Peloton either needs to evolve as a company by strengthening its balance sheet and being profitable, but in its current state, these kind of results are not viewed positively.

Before moving on to the positives let’s confront the main problem with these results. Companies like Peloton were for some period of time strong investments for those who are willing to take on more risk for extremely high growth potential. Now that Peloton has stumbled and now is looking at more modest growth in the future does the thesis still hold? The answer will depend on how Peloton executes and we will not know until after a few quarters of results. Can Peloton evolve as a company to sustainable growth or will it suffer more trying to recreate its “glory days”? Capital was cheap a few years ago and companies could afford to burn cash to enable growth. Now, this is not the case and companies set up like that will fail. Now the advantaged companies are those with fortress balance sheets, strong profitability, and cash flow. Peloton faces challenges on all three of these fronts.

This is not a time where valuations simply reset. The organization of what it takes to be a successful business has changed. Peloton needs to focus on having free cash flow and then growing it to be on a path to prosper in this new setting.

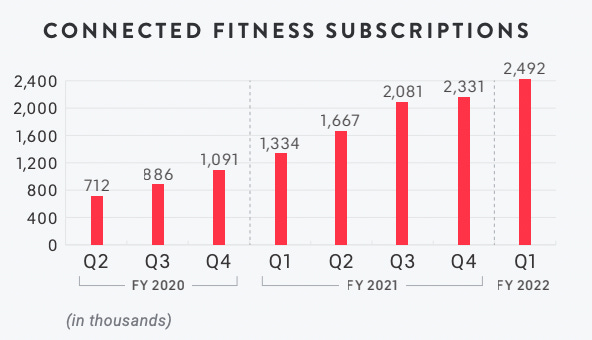

Now on to the positives, which there are multiple positives from the Q1 2022 earnings. Despite Connected Fitness Revenue being down year over year (Y/Y), the Subscription Revenue is up 94% Y/Y. Importantly, the stickiness of the service is also up with 120.5m workouts completed in the quarter 55% up Y/Y. Again this is down from the previous two quarters. On the bright side, most customers end up staying with Peloton subscriptions (low churn) because once someone spends upwards of $1200 on a bike they aren’t going to just not use it. For their Connected Fitness Subscriptions Peloton boast just 0.82% churn rate for Q1 2022 and a 92% 12-month retention rate.

Source: Peloton Q1 2022 Earnings Report

Company Outlook

Management has made changes that have increased the near-term pain within Peloton’s recent results, but they have set it up for a stronger future by focusing on subscriptions. For example, lowering the price of bikes in August hurt mainly Q4 2021 and Q1 2022, but allowed for more people to purchase a bike. This is important because it changes the focus from the product to the service as Peloton now moves towards a future where more returns are made on the Subscriptions than the Connected Fitness portion of the business. Also now the goals set for future quarters and end of year are all focused on increasing subscribers, limiting churn, and increasing gross margin (Hint: those will go hand in hand). This would also be an important asset in the case of a possible acquisition by a deep-pocketed tech player like Amazon, Apple, or Google. All mega-cap companies involved in streaming could capitalize on this alternative streaming market.

Peloton also wants to optimize itself as a streaming or SaaS company (subscriptions) because of the better margins, compared to the margins from bikes and treads. In Q1 2022 Peloton reported a 12% gross margin on Connected Fitness Equipment and 66.7% gross margin on Subscriptions. This is also an area Peloton has set as a target to improve on and Subscriptions could fuel this improvement.

Peloton also has been burning cash at a worrying rate, with ~$800m loss in cash over the past year. If this spending continues the company has just over a year of cash currently ($879m). It is important to realize a portion of this cash was put into inventory which makes this less extreme. Now, this cash-burning is even worse as capital has become expensive again. Analysts have said they expect Operating Expenditures to decrease by $165m in the second half of this year and $450m next year.

Cash flow has been consistently negative, but Peloton expects to have positive Free Cash Flow next year. This will be done by improving margins on Connected Fitness Revenue, growing the subscriber base, selling the land and facility for manufacturing in Ohio, and finally moving the inventory to turn it into cash for next year.

Competition

SoulCycle is the closest comparison and competitor for Peloton. SoulCycle has been advantaged in returning to normal movement as they do run in-person training facilities. However, they also have built an app under the Equinox+ umbrella (their parent company) that is an equivalent to the Peloton App. They have gone with an inverse strategy to Peloton for pricing. A SoulCycle bike is $2,500 starting price and the subscription is $40/month. By having such a high price this discourages buying (especially with Peloton with a comparable product at less than half the price) and hurts their subscriber numbers.

Insider Ownership

Strangely given the large price pullback – from $162 per share to $9 per share – there hasn’t been any recent insider buying. Some sales have occurred. Other C-level executives have liquidated recent option awards including the Chief Financial Officer, Chief Product Officer, and Chief Supply Chain Officer. CEO and Co-founder John Foley has been selling shares here and there throughout the year, but these seem to be connected to stock compensation, he still retains the majority of his shares accounting for a ~2% stake of the company.

Valuation

“No matter how great it is, it’s not worth an infinite price”

– Charlie Munger

Growth companies are judged in part by the Rule of 40: A company's revenue growth rate plus its profitability margin should be greater than 40%

Until recently Peloton had been trying to grow revenues while also not maintaining high-profit margins. Now Peloton has taken some hits to growth and profitability, but these have the potential to actually help build it into a more quality company (in the long term). With Y/Y revenue growth at 6% for Q1 2022 and a 32.6% gross profit, Peloton scores a 38.6%, it doesn’t pass. This is an important difference because in previous years Peloton was often well above the 40% threshold. Peloton has taken a hit to growth but hasn’t been able to counter it with fast enough growing margins. Unless Peloton can show better value by actually having earnings and cash flow this is one of the best ways to value it.

From a valuation, perspective Peloton was hit harder than necessary and a bear market on top of that makes it looks pretty enticing. For reference, it is currently trading at 1.04x Total Enterprise Value / Revenues. Since it is a growth company that has been going through a rough time (not producing any earnings) statistics like Price/Earnings are not useful. Overall it does seem undervalued based on the information we can interpret. For another reference point Price/Sales was at 6x pre-pandemic and now is hovering at 0.86x. There is significant, but this seems like an unnecessarily low valuation.

The company is risky as it is set up to be a high-growth business, but the focus moving forward is in the right place and management seems to be realistic about expectations while also striving to maximize situations and have been doing a good job of damage control (in spite of what the market shows). In my opinion, Peloton is on its way to becoming the highest-quality version of itself yet.

On the bear side, the cores to good investments are cash and profitability. These are two things that as of yet Peloton has not been able to achieve. This is a difficult switch to make and may cause more sell-offs as its majority of growth-focused investors lose interest. Strong execution with streaming could solve this, but that is no easy feat.

Until Next Time,

Soren

Exer-cycles were never sexy. Take them out of the equation. Would you pay $44 / month for Disney+? Amazon Prime content? Me either. So this bodes Ill for Peloton. At least folks have a nice clothes hanger after they cancel their subscription.