Owners Not Bankers: HIFS Annual Meeting (Issue #92)

“Think of ourselves as owners first, not bankers”

- Patrick Gaughen, COO & President

The managers at Hingham Institution For Savings (NASDAQ: HIFS, “Hingham”) are the first to admit last year was a sub-optimal performance for the company and as the largest individual shareholders in the business would like to improve. That being said a not good year for Hingham isn’t as bad as it seems. For example, the typical high 10s or low 20s ROEs for Hingham are rare in the industry. In this particularly poor year of 2023, the company produced 6.57% which is the industry average, but as President and COO of Hingham Patrick Gaughen says, “[it’s] not acceptable for us.” This a prime example of the Kaizen, pursuit of continuous improvement, approach Hingham has towards banking. Similarly to the ROE, the efficiency ratio significantly deteriorated almost tripling to 57.18%. Again this is still strong for the industry but Hingham holds itself to a higher standard. During this time, they have had a 13.6% CAGR on book value and deposits have had an 8.4% CAGR. As mentioned by management deposits growth needs to increase in order to sustainably grow book value.

Profitability has been down this year and last year from a peak in 2021, but a lot of that is due to realized and unrealized losses from the equity portfolio. This is clearly a factor of the large gain during 2021, a positive outlier year for most stocks, and now a large decline for 2022 and 2023, two negative outlier years for most stocks.

Interest rate changes and cycles are only problematic for banks if there are swift increases. The short-term Net Interest Margin (NIM) compression is a hit to performance, but in the long term, Hingham can regain their profitability and advantage. This should also be a warning to investors and followers of Hingham in case there are quick interest rate drops to not be overly enthusiastic from the short-term increased margin.

Hingham still has a rock solid balance sheet. The commercial loan portfolio is $3.5bn and contains ~1,700 loans. Of these loans there are no non-performing, delinquent, or modified loans. This is extremely impressive. Further, of the entire commercial loan portfolio there is only one past due payment on a $460k loan as of the meeting. Management went on to mention that the slides were made the day prior to the meeting and that the client likely could have paid since.

“We are not in the business of modifying loans”

- Patrick Gaughen, COO & President

Additionally, most of the expansions of the team were into building the digital banking team and more relationship managers for onboarding new customers. While Hingham focuses on not doing a lot of different activities they try to be very good at the things they do. Having strong relationships with clients and customers is a priority for the company. This was a driving factor in investing to teams to improve and uphold their level of service.

There was a lot of focus on buybacks at the meeting. Management said that typically they lean more towards special dividends or reinvesting into organic growth. Since, Hingham doesn’t have a holding company meaning all buybacks need to be approved by regulators. Buybacks can also be a supplement to investing in organic growth. Dividends and special dividends are often a more direct way to give value back to the investor. This has less regulation hassle and we have seen it often be a preferred method of shareholder appreciation with the almost annual end of year bonus dividend.

This is one of the most underrated annual meetings. It is always great to see the same people coming back year after year and even better to see some new faces. I really enjoyed reconnecting with everyone there and I am looking forward to the next meeting. Berkshire is also coming up later this week. If you are interesting connecting with me feel free to reply to this email or reach out directly at soreninvesting@gmail.com

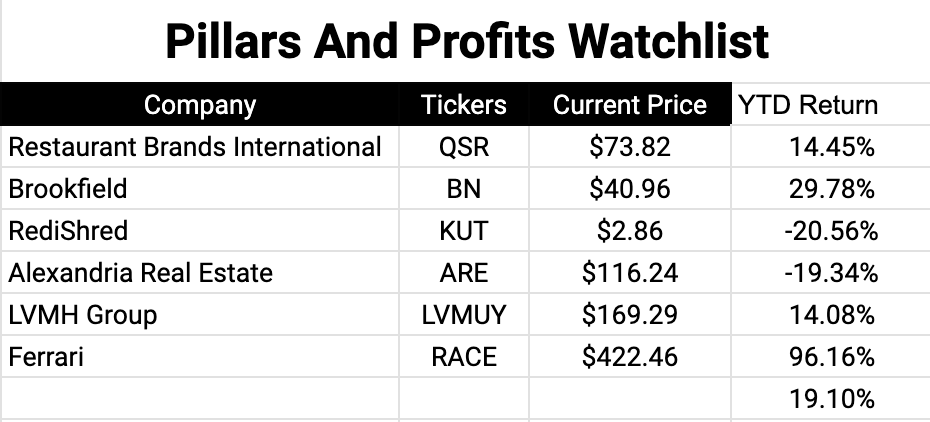

Watchlist Update:

Portfolio Update:

Until Thursday,

Soren

Planning to go to Boston on April30th for the annual meeting. Things are improving. Any insight on how to attract more déposits and trickle down the unbalance between loan and deposit