Markel's 3 Engines For Success (Issue #26)

Pillars:

Competitive Advantage – Created a “Blue Ocean” in insurance, investing, and ventures through long-term focus

Fortress Balance Sheet – equity and ventures investments are safety first

Growth – Each of the engines have strong growth metrics

Long-term Focus – Investments are never planned to be sold

Capital Allocation and Operation Skills – The 4 avenue capital allocation “flow-chart”

Undervalued In Context – Each piece is valued close to their intrinsic value

Markel has been referred to as the next Berkshire (seems like we hear that a lot lately). The comparison goes even further as Berkshire refers to itself as “groves, Markel’s management thinks of itself as three engines. For example, if one is not doing as well then the other two can power the business forward. The first engine is specialty insurance then investments and finally Markel Ventures. Like Berkshire, Markel focuses on rational capital allocation with a long-term in all of its investment engines and likes to keep things simple and safe at all times. The approach is simple but can be difficult to maintain.

Markel Co-CEO Tom Gayner likes to tell the story that he learned early in his career- if you want to avoid investing in companies that are run by crooks then avoid buying companies with a lot of debt. It is not that all companies that have debt are run by crooks, but if you were a crook then one thing you would likely do is take on a lot of debt. Markel is built up on many similar simple guiding principles that eschew excessive risk-taking in favor of safer, sustainable profits over long-term time horizons. The company does not shoot the lights out for a year or two and then have an awful year, instead, it is a steady eddy compounder, grinding out incremental improvements year over year.

Gayner learned investing early on, his father told the story of a couple in his hometown who received stocks as a wedding gift. They were new to investing, and they went to the richest person in town, who owned the furniture store to ask how do they sell stock. The main replied, “I don’t know - I’ve never sold any.” Markel’s insurance business goes back over 100 years, and many of Markel’s stock holdings go back decades, this is a company built to prosper well into the future and the future is what investing is all about.

Insurance

Markel has been an insurance company since the beginning. More specifically the company is involved in specialty insurance. These are things like bass boats that have engines larger than they are rated for, high-performance offroad vehicles, or any other risky vehicles, event insurance, antique cars, small businesses, and summer camps, are just some of the types of niche areas that Markel operates in. They are not trying to compete with standard insurers. Instead, Markel works to insure special situations that other companies won’t. They have created a blue ocean of sorts within the insurance industry and it allows them to charge higher premiums than standard insurers who do not compete in this space. This allows the company to charge high premiums because of the risk and low amounts of competition. Markel is an insurance company at its core. This business is still growing with 20% increases in net premiums written year/year in Q2 2022. 9% of that growth is accounted for in price increases. This demonstrates the power of the niche Markel resides in. Gross written premium has more than doubled from 2017-2021 going from $5.5bn to $11.4bn.

Insurance made $6.5bn in earned premiums in 2021 accounting for half of Markel’s total revenue.

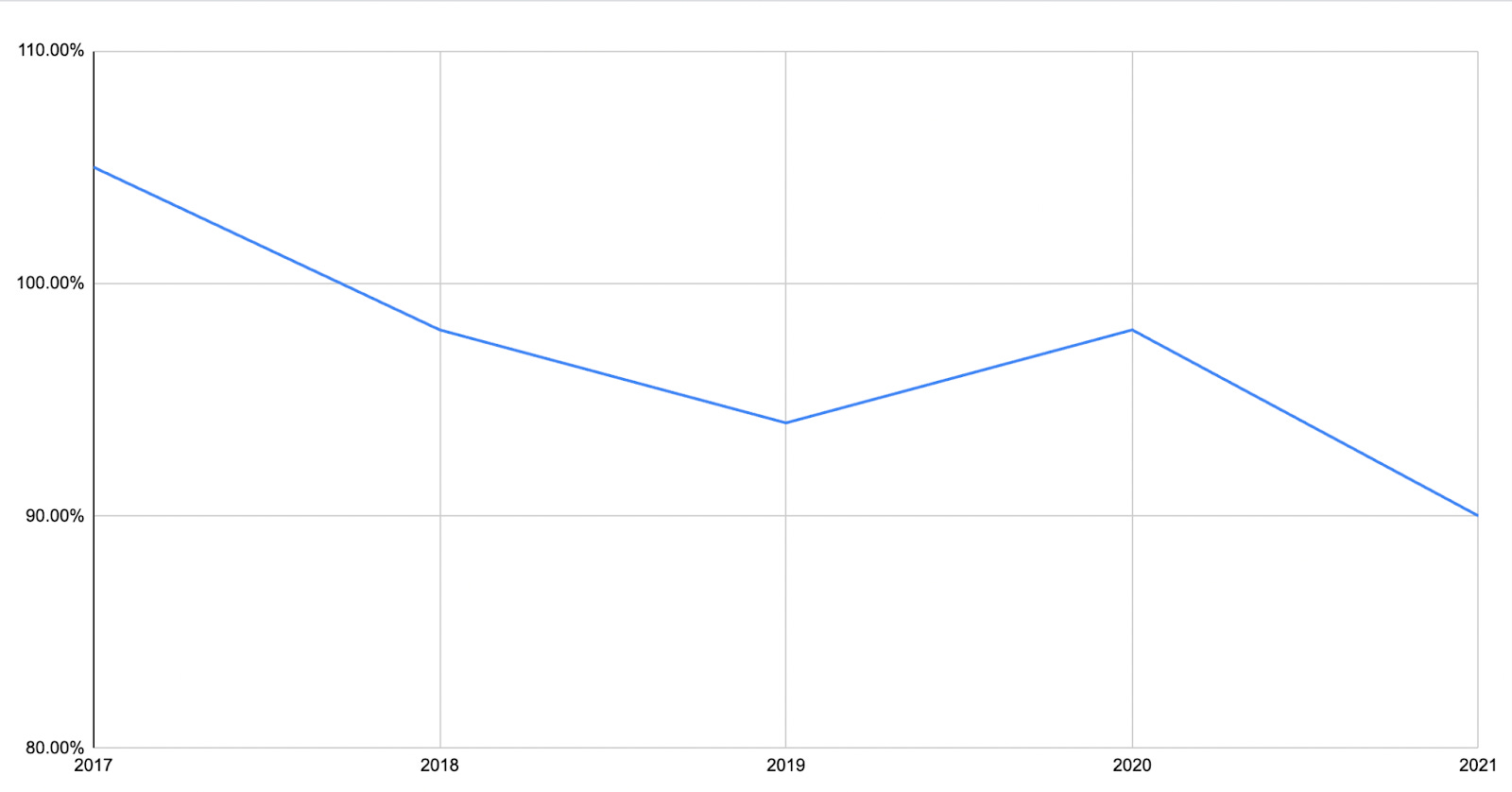

A key statistic in insurance is the combined ratio which measures losses and expenses divided by earned premiums meaning the lower the better. Markel’s combined ratio over Q2 2022 was 91% and $1.8bn in earned premiums. This was up from 87% and $1.56bn in Q2 2021. The higher combined ratio is worse, however, the increase in premiums earned is positive.

Combined Ratio Over 5-year Period

Investments

While most insurers focus on investing their float in bonds, Markel focuses on investing it in equities and privately held businesses and compounding it over the long term. They do this through their other engines: Investments and Ventures.

Now on to the investment side of the business. Markel Co-CEO Tom Gayner runs the investments side. He’s been a part of Markel since the 80s and worked his way up to his current position. His investment style focuses on holding quality businesses forever. There are no short-term investments or quick exits, but long-term partnerships with businesses. Some years back, Gayner said he likes to stay around hs circle of competence which he then described as “sugar, money, and dirt” since then he has branched out.

Markel has a total of 121 stocks in its equity portfolio. Here are the top 10 by percentage:

Berkshire Hathaway (BRK) 12.5%

Brookfield Asset Management (BAM) 5.5%

Alphabet (GOOG) 4.3%

Home Depot (HD) 3.6%

Diageo (GEO) 3.4%

Deere & Co. (DE) 3.2%

Amazon (AMZN) 3%

Visa (V) 2.7%

Walt Disney (DIS) 2.7%

Apple (AAPL) 2.4%

Interestingly the investment focus seems almost count intuitive to the insurance focus. While the insurance side focuses on some of the most interesting, exciting, and scary items to insure the investment side looks for the most mundane and boring businesses. For example, John Deere tractors or Brookfield Asset Management, a company to prides itself in its safety. However, they have moved beyond sugar, money, and dirt and are also open to tech companies with Google, Amazon, and Apple all in the portfolio. They did pick the three safest companies possible as their exposure to the sector. Safety and simplicity remain hallmarks.

Ventures

The third engine is Markel Ventures. Markel Ventures owns companies like Brahmin handbags, Buckner Heavylift Crane, Captech, and more companies. Ventures is built up of many different companies, but as they state they seek to be the best at what they respectively do. The focus as with the rest of the business is long-term (a Pillar).

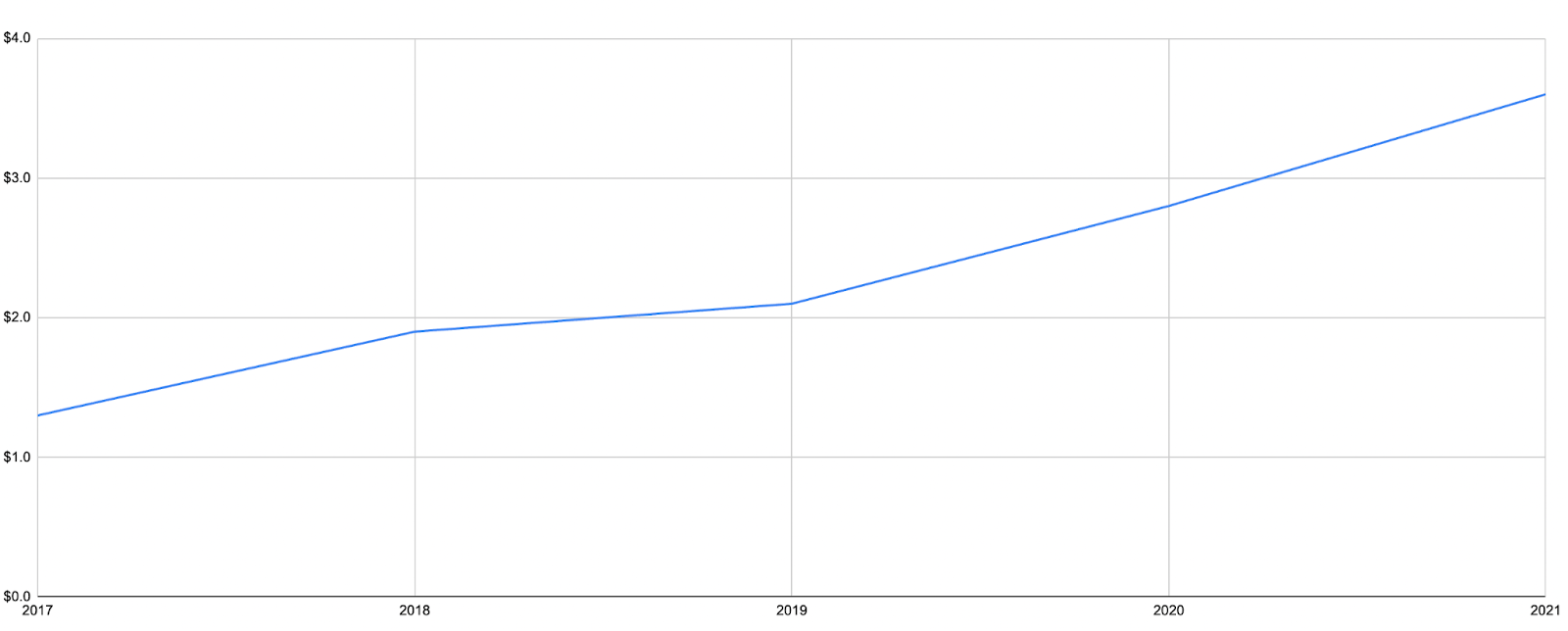

Ventures made ~$3.6bn in revenue in 2021 accounting for just over a quarter of all of Markel’s revenue. Revenue has grown from $1.3bn in revenue from 2017.

Revenue From Ventures from 2017-2021

The businesses comprised under this branch are not like private equity where they will be quickly sold or spun out. Instead, they only acquire businesses that they plan on holding forever. This means companies under this portion of the umbrella are more incentivized to win in the end than in the long term.

While some of the ventures are more exciting there are still some mundane businesses like Ellicott Dredges which dredges canals and channels. This keeps with the themes of the investment branch.

In 2021, Ventures acquired a majority stake in both Buckner Heavy Lift Cranes and Metromont. Buckner’s cranes are the largest domestic cranes available and can up to 2000 tons. Metromont is the #1 producer of precast concrete in the southeast. Both of these businesses take a lot of physical movement of heavy objects meaning they are unable to be replaced by the internet. Ventures revenue are already up to $2.26bn so far this year. This is a strong increase considering all Ventures revenue in 2021 totaled $3.6bn.

Similarly to Berkshire Markel Ventures is not looking to rebuild or restructure most of the businesses it acquires. Instead, they let management continue their course under the company.

Gayner on Capital Allocation

The first place Gayner focuses capital is easy or nearby expansion. These are simple additions to services in insurance or ventures that create value for the company. The next place is acquisitions of insurance companies or ventures. Then purchasing public equities. Finally, buying back stock if it is at a favorable price. Markel bought back ~100,000 shares in the first half of 2022. That is the standard flow Gayner uses to decide where to deploy capital. Sometimes multiple are being funded at the same time (even all). The capital is used in one of or all of these avenues how it rationally makes the most sense.

Valuation

The combined total of the holdings in the equity portfolio alone are worth ~$7bn. Further, Markel sits at a comfortably low 1.32x Price/Book multiple. While this is a good metric for insurance like I mentioned in the Boston Omaha Write-Up this is no longer a good statistic to measure companies of this type.

Investment Thesis

Within the company, the investments have an emphasis on safe growth and the insurance focuses on calculated risks. At the same time, this is all at a very low valuation making it a strong holding in the portfolio.

The insurance engine will continue to grow and create more capital to be invested in the 4 capital allocation avenues. As they progress in their insurance niche they should be able to continue to raise their premiums as well as expand their reach.

For the equity portfolio, the investments are very safe, but also strong long-term growth opportunities that will be subject to compounding. The value is simple to measure and makes it the most straightforward engine for analysis from an outside investor perspective.

Finally, Ventures will not reflect their value as well on the balance sheet, but an idea of the engine’s success can be measured through revenue growth. Ventures which has been around since 2005 is still growing quickly with 2 large acquisitions so far this year. Now it has become an important part of the Markel umbrella.

Until Sunday,

Soren

Disclaimer: Soren Peterson and Pillars And Profits Newsletter are not responsible for any investment results. This is not financial advice. Always do your own research.