LVMH Group: The Owner Of Luxury (Issue #48)

LVMH Group: The Owner Of Luxury (Issue #48)

Background

Louis Vuitton Moet Hennessey (LVMH) is a conglomerate of 75 top-tier luxury brands that have over 5,500 stores worldwide. These are not just expensive brands either, they are world-renowned brands that have in many cases been around for over 100 years and have the highest quality reputations and price points. . LVMH Group was formed when Louis Vuitton and Moet Hennessey merged in 1987. LVMH is controlled by the Arnault family with the current CEO of the company being Bernard Arnault who orchestrated the original merger in the 80s and continues to make accretive acquisitions that widen the LVMH moat. We will talk more about the Arnault family later in the deep dive.

Company Overview

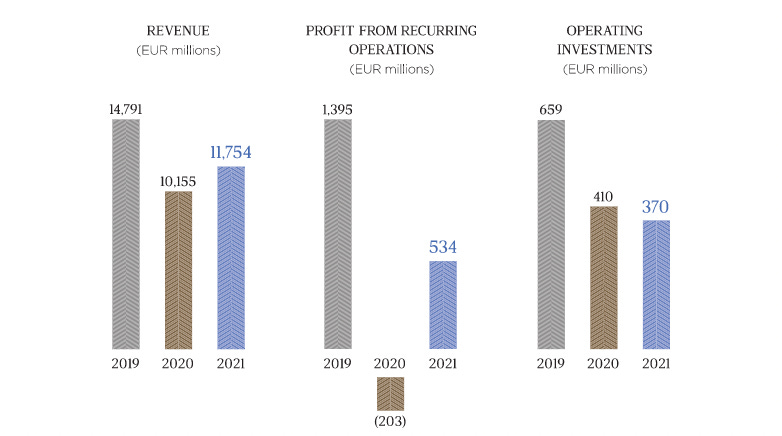

LMVH group reported 79.2b euros in revenue in 2022 ($86.1b). This is up 17% year/year the same as gross profit at 14.08b in 2022. Now the company is listed as the highest-value company in Europe. This has also powered Bernard Arnault to overtake Elon Musk as the richest person in the world.

“During difficult years, whether that’s for macroeconomic or geopolitical reasons, the LVMH group takes market share and progresses, which has been the case since 2019.”

Bernard Arnault, Chairman and CEO of LVMH Group

Consumers of these astronomically expensive goods have enough money to remain, loyal customers, no matter the greater economic climate. The evidence here is that 2022 was a very difficult economic year across the globe including inflation, layoffs, and other stresses, meanwhile, LVMH delivered a record performance in 2022 with revenue and profits up 23%.

LVMH sells through multiple channels. First through their own stores that they operate. These are around the world and often combine multiple of their brands that work well in tandem. Next, many of the brands can be sold through stores that combine multiple products. For example, TAG Heuer can be sold through watch stores that have multiple different brands. Finally, online sales are another revenue source, however, many like to go in person for the customer experience and to see pieces before spending significant sums on them. Like Ferrari, LVMH is very selective in retail partners and refuses to work with Amazon although their products are often resold on the site.

LVMH’s 75+ brand businesses are split up into five categories: Fashion & Leather Goods, Wines & Spirits, Perfumes & Cosmetics, Watches & Jewelry, and Selective Retailing. This way you can see how each sector or area within luxury is performing compared to the rest. This tracking method reflects trends in the category overall and is much more simple than 75 mini breakdowns.

Fashion & Leather Goods

This is the largest business unit and also provides large margins. In 2022, it produced 38.6b euros in revenue which is a 25% year/year increase. Dior specifically is a growth brand for this branch of the business. There is some growth potential for Celine, Loewe, Fendi, and Loro Piana. Unlike Wine & Spirits, the largest market for these goods has been Asia accounting for 50% of all sales. 9% of all sales came from Japan alone.

Wines & Spirits

In 2022, the company sold ~83m bottles of champagne, a 24% year/year increase, and ~117m bottles of cognac, a 14% year/year increase. Wines & Spirits produced 7.1b euros in revenue which is a 20% growth year/year. Many brands like Moet & Chandon, Hennessey, and more under this section of the umbrella hit all-time highs in both the US and European markets. This is one of LVMH’s older business sectors meaning it is not meant to be a growth area, instead it has steady growth and makes high returns which allows for more acquisitions.

Perfumes & Cosmetics

A key portion of this luxury conglomerate Perfumes & Cosmetics generated 7.7b euros in revenue a 17% increase year/year in 2022. Even though Asia accounts for more than half of sales for this part of LVMH it is still the company’s main focus for future growth. A key going forward will be making many of their brands fully global and not just in the European markets.

Watches & Jewelry

This part of LVMH has seen the most growth as it almost tripled year/year and more than doubled pre-covid numbers with 10.5b euros in revenue an 18% increase year/year. Similar to Formula One’s recent increase in popularity and revenue many luxury watch brands are connected to Formula One teams and could be benefitting as well. 2021 and 2022 World Champion Max Verstappen wears a Tag Heuer (owned by LVMH). Another similar theory is the increased popularity of international soccer as a product of the World Cup where luxury watch brands are also heavily connected. 25%of sales are from the US and 47% from Asia (11% from Japan alone).

Selective Retailing

This branch includes brands like Sephora, DFS, and other luxury retailers. Revenue for 2022 was 14.9b euros which is up from the previous high in 2019 of 14.7b euros. This is also a 26% year/year increase. The US is the largest market at 39% and Asia second at 24% (excluding Japan). Not very surprising based on how retail stores in general have been giving way to online ordering. Further, US and Asian markets have been seen to order more online than European markets.

Source: LVMH Group Annual Report

Figure: Percentage of revenue from each branch of LVMH (author’s calculation)

Acquisitions

Acquiring and business transactions have been Bernard Arnault’s real strategy for success. Even though the brands go back centuries, the LVMH Group is relatively new. The company of LVMH Group was started with a merger of Louis Vuitton and Moet Hennessey in the 1980s. Since then LVMH has grown by acquisition to 75 brands and they’re not done yet. Some of them include large acquisitions like Sephora and Tiffany’s & Co. The Tiffany’s purchase occurred in 2021 and earnings from the company have since doubled. Now the company will break the billion-dollar (euros) mark in profit. LVMH and Arnault paid 30x net income of 2019 at $16b, but that becomes a value investment at now ~15x with the improved earnings. Other big acquisitions include Sephora for $200m in 1997 and Bulgari for $5b in 2011. Sephora now makes 10b euros in revenue and Bulgari now produces ~5b euros in revenue each year.

LVMH has created a luxury vertical integration that allows them to market and sell these products much better and more efficiently than other sales sources. This means they can purchase brands and immediately boost their prominence and sales.

Succession

No, I don’t mean the TV show. All jokes aside succession is a significant part of the future of this and many other businesses that have a key manager who built up a large company and is not towards the end of their career or life. We are seeing this in Berkshire Hathaway with Warren Buffett (92) and Charlie Munger (99) as well as here with Bernard Arnault (73). For LVMH there is currently a structure of “heirs” who run respective pieces of the conglomerate for many years now. This gives them experience in the business and multiple potential individuals to take over. Personally, I think they should remain as heads of separate parts and collaborate to run the company together. It will be important going forward how succession is structured and communicated.

Daughter and eldest child Delphine Arnault (47) is the current Chair and CEO of Dior and executive vice president of Louis Vuitton. She is the favorite to run LVMH post Bernard. Other related managers include, Jean at just 23 and fresh out of MIT is already CEO of the Watch branch of LVMH. Meanwhile, Jean’s older brother Frederic (28) CEO of TAG Heuer works under Jean. Antoine (45) was the Dior CEO before Delphine and now operates as Vice Chair of the brand as well as CEO of Berluti and Chair of Loro Piana. Finally, Alexandre (30) was CEO of Rimowa (starting at 25) and now is Executive Vice President of production and communication for Tiffany & Co.

Valuation

LVMH Group may be a luxury brand or brands but it trades well below those usually high multiples. The company is closer to a value investor realm at ~22x Price/Cash Flow. However, the multiple is higher at 7.41x Price/Book but this is still not unheard of.

LVMH owning luxury brands means it has high returns and margins. This means they have a lot of cash to work with. Management luckily puts this towards things like buybacks and dividends. For example, the company pays a 1.46% dividend and bought back 0.33% worth of shares in 2022.

Investment Thesis

LVMH is a good long-term growth opportunity and investment because it has 4 ways to grow. First, the businesses have steady growth over time. Second, acquisitions of additional luxury brands are powered by the high returns from the existing brands. The last two are my favorite 1, 2 punch combo for great returns buybacks and dividends because the dividends become more valuable as buybacks continue. On top of all this, the company trades at a reasonable valuation for any company not to mention one in the luxury sector.

Until Next Sunday,

Soren