It's Time To Buy Banks (Issue #84)

Happy Thanksgiving to those who celebrated!

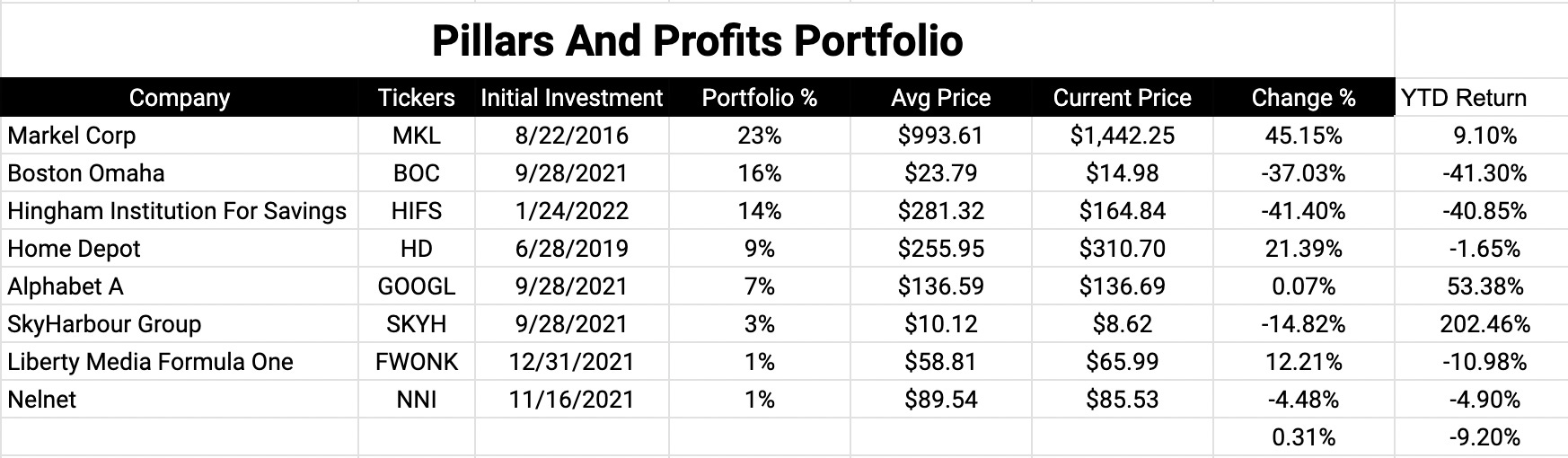

Banking is a fascinating industry to analyze and follow, however, it is rarely a good time to actively buy bank stocks individually. This is why I only hold one direct bank stock in my portfolio (Hingham Institution For Savings).

This is the best time to buy banks.

Banks for the first time since the pandemic are in a state of virtually universally low valuations. Banks usually don’t get moved by waves as much as tides typically, but that tide has gone out enough to affect banks. High interest rates are disincentivizing new loans on the front end and increased interest rate payouts for depositors on the back end are punishing banks. Conversely, well-run banks with good management can make it through difficult times.

Most dedicated bank investors find the highest quality banks they can and then set seemingly absurdly low multiples for any purchasing action. But when times seem dark for banks the valuation multiples often drop because the shares get sold off with little movement in the core of the business.

Hingham Institution For Savings (NASDAQ: HIFS — $355.63m) is at the forefront of well-run banks and seems to be a repeating theme for active followers of this newsletter. The bank is a prime example of quality for a number of reasons but now it is also at a discount. Currently trading at 0.89x Price/Book it is a bargain. For more details on the understanding of this bank check out my post on it here (note: this was written at approximately double the current price).

Although the banking industry is suffering from net interest margin compression they are still valuable businesses and they are in an enduring industry.

Thrift Conversions:

There are many different ways to get invested in banks. A very different bank investing genre is Thrift Conversions. This is a very different style of investing and only works on community banks that go public, however, the niche is interesting enough to warrant a place for conversation on the topic. Use the button below to join in on the conversation.

Watchlist Update:

Portfolio Update:

For access to the full spreadsheets and linked deep dives go here.

Until Thursday,

Soren

Disclaimer: Soren Peterson and Pillars And Profits Newsletter are not responsible for any financial results. Soren Peterson and Pillars And Profits Newsletter are not financial advisors. Nothing enclosed in these newsletters is financial advice. Always do your own research.

Hi. Thanks for the original write up on hingham.Are you concerned about Hingham having to keep increasing its borrowing/advances from FHLB? I just reread the 10-k last night and saw it looked like last year it’s average rate it was paying to FHLB for advances was higher than its average rate it had for it’s written loans. The last 10-q showed its advances had increased again to 1.5 billion with a max cap around 2 billion. Can Hingham increase that 2 billion cap if their written loans keep increasing at a much faster rate than their deposit base?