HIFS Earnings Were Disappointing Or Not (Issue #70)

HIFS Earnings Were Disappointing Or Not (Issue #70)

With Hingham Institution For Savings (NASDAQ: HIFS — $m) I struggle to...

As a newsletter writer my job is to look at information and summarize and analyze it. With Hingham Institution For Savings (NASDAQ: HIFS — $469.22m) I struggle to comment in a productive way. Because of this I am going to write with two different voices. The HIFS Sympathizer and the HIFS Doubter. Agree with either or neither. I don’t want to come across as someone who doesn’t understand the risks of banking (which are many and massive), but I generally trust the management team and have confidence in Hingham as a company.

Here are the facts:

Net Income increased ~2.6x year/year to ~$8.2m for Q2 2023

8.27% ROE and 0.80% ROA for Q2 2023 compared to 3.43% and 0.34% for Q2 2022

Core Net Income (Excluding Securities Gain/Loss) down ~73% year/year to $4m for Q2 2023

4.06% Core ROE and 0.39% Core ROA for Q2 2023 compared to 16.42% and 1.63% for Q2 2022

8.47% ROE and 0.81% ROA for first 6 months 2023 compared to 8.20% and 0.83% for first 6 months 2022

Net Income increased ~12% year/year for first 6 months 2023

Net Interest Margin decreased 193 bips year/year to 1.28%

0% non performing assets and charge-offs

55.03% Efficiency Ratio from 21.30% Q2 2022

HIFS Sympathizer:

While these are not the growth numbers we have historically seen Hingham chose to take the performance hit as opposed to trying to squeeze out a more favorable short term result that could pose long term threats. Net Interest Margin compression is real and the bank felt the strain, but, as I have been saying, Hingham underperforming would still be a record year for the average bank. For example, their Efficiency Ratio up to 55.03% from 21.30% a year ago is significant, but 55% for many banks would be a solid year. Further, the ~8% Core ROE is not great for the bank, but again would be commendable for a non-Hingham bank. The ROE for the first 6 months of the year is also more consistent with results from the same period last year.

Finally, Hingham had no non-performing assets or charge-offs. For those less familiar with the operation Hingham’s charge-offs have rounded to zero for the passed 20+ years, including 2020 when they climbed to $240,000 on a ~$4bn loan book (the following year they were $1,200).

HIFS Doubter:

Hingham’s performance in this quarter year/year is subpar. They are truly feeling the effects of net interest margin compression. The bank’s efficiency is being majorly hit. What was once a key strength of theirs is now becoming a weakness. The existing loan portfolio may be solid with many safe loans that rare don’t perform or charge-off, however, looking forward there will be fewer short term opportunities to meaningfully grow the loan book.

On a larger scale this is not a time for bank investing. There is too much pressure on the already tense environment.

“Banking is business in a pressure cooker.”

I personally agree more with the HIFS Sympathizer view, but I hope I was able to at least partially shed light on the anti side as well.

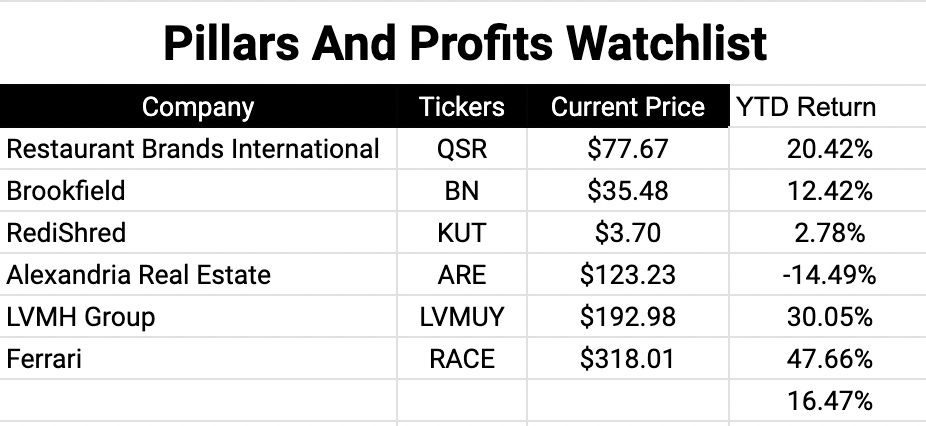

Watchlist Updates:

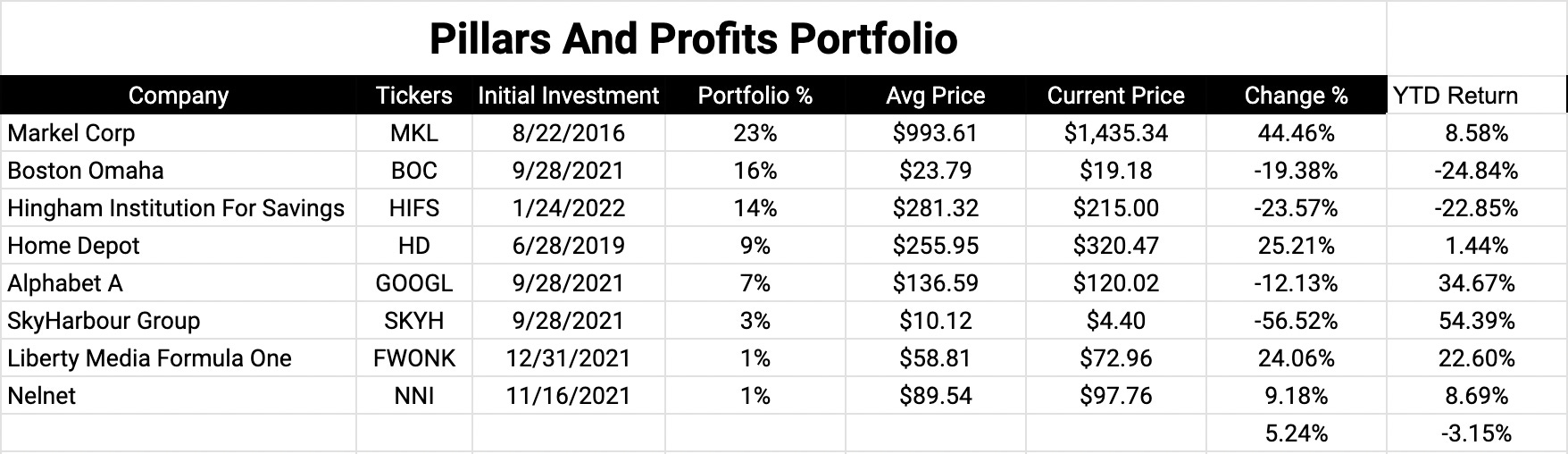

Portfolio Updates:

To access the full spreadsheets and linked deep dives go here.

Until Thursday,

Soren

Thanks for the article. It would be great if you can comment on 3rd quarter results as well.