Digital Is Key To The Flywheel Of Banking (Issue #90)

Digital Is Key To The Flywheel Of Banking (Issue #90)

Digital Is Key To The Flywheel Of Banking

A well-executed digital banking strategy can open up growth opportunities for banks and bypass the typical and capital-intensive means of expansion: new branches, large hiring waves, attracting and retaining loans, and deposit growth. Digital/mobile banking offers efficient ways to engage with customers. We’ve already seen the emergence of online banks in a number of forms. Banks of all sizes and large technology companies will all be competing but they all can’t do everything. More importantly, they can’t all do everything well. Small and specialized banks have the potential to expand their reach within their niche. Medium or small-sized banks can pick the most important focus for their customers and leverage those tools or offerings in the digital/mobile space. Used effectively, small and midsize banks can use digital/mobile applications as both a threat to other banks and a moat against being wiped away by a larger counterpart. The key to banking is consistent and constant innovation without overextending and staying true to the core.

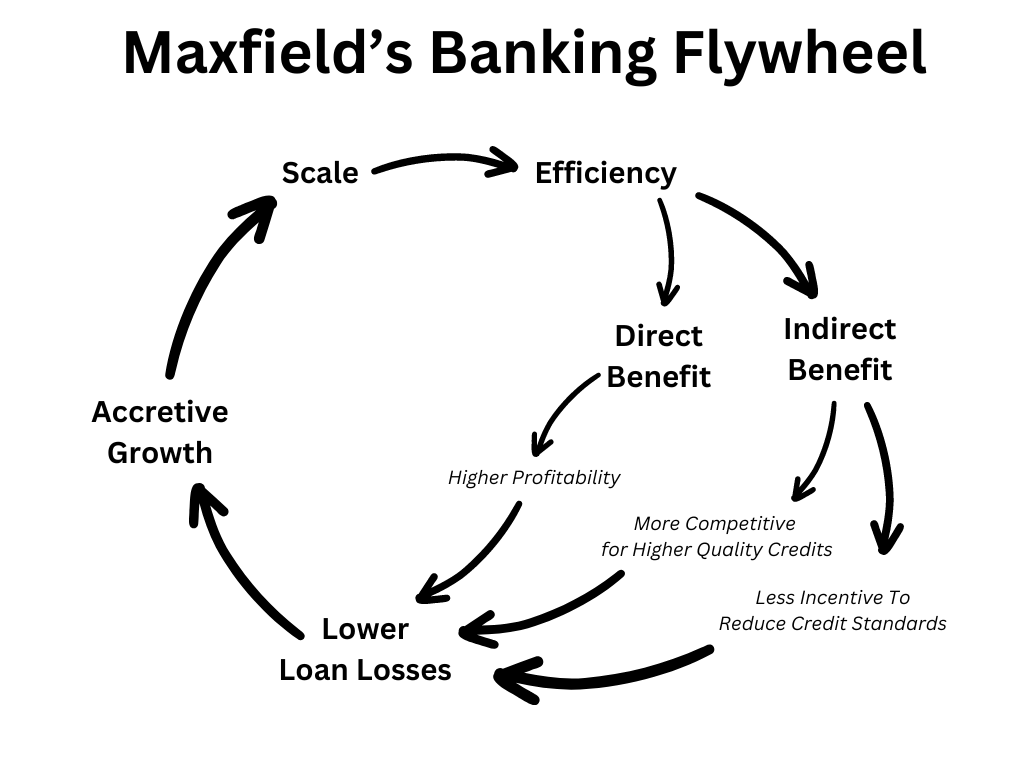

“The Flywheel Of Banking” is a framework created by John Maxfield(1) to describe a network of factors that work to accelerate growth, expansion, and overall improvement in banking. The flywheel effect compounds to contribute to significant changes.

Maxfield’s banking flywheel starts with efficiency; this has a two-pronged effect. First, there are clear and direct benefits like a lower Efficiency Ratio, higher profitability, and a more premium valuation. Second, there are indirect benefits that come from the increased efficiency. For example: the ability of a bank to compete on loan rates results in attracting better customers. Better quality customers beget increased profitability which results in credit standards that don't have to be lowered to hit revenue and profit targets. Sometimes credit standards can even be raised. With better quality customers come lower loan losses. Lower loan losses combined with the direct benefit leads to accretive growth. Scale is the last step of the flywheel. When the growth engines work together, banks can grow and potentially scale from a town into a region or state, or from a state to a multi-state region or even nationwide. Scale creates more growth opportunities thus, the flywheel cycle begins again.

Maxfield’s Flywheel is a very useful mental model for the business of banking. What happens when we overlay potential changes from digital and mobile banking onto the Flywheel?

Digital and mobile banking is unlikely to alter any of the longstanding banking objectives expressed in Maxfield’s Flywheel, but rather offer some new means of achieving them. At the same time, digital and mobile reshapes the competitive ecosystem and bring some fundamentally new competitors that may disrupt the order of things in the banking world.

Banks need to think about finding a digital and mobile strategy where they are on offense (unlocking new advantages through technology) and where they are on defense (coping with new powerful competition) at the same time. Let’s jump in.

Digital and mobile integration very clearly connect to and enhance many of the parts of the flywheel. We’ll dive into each connection to see where opportunities and threats emerge, and how banks can find ways to navigate through these changes.

Navigating the Challenges of Digital and Mobile Banking Summary:

Opportunities:

Creating leadership in the Digital/ Mobile Space

Efficient, Scale, and Growth

Digital/Mobile at the Center of Customer Relationship

Threats:

Managing Risks

Blending Culture

Evolution or Extinction

Navigating the Challenges:

Developing Digital/Mobile Strength

Learning with Analytics

Capital Allocation

Digital and Mobile banking will be key to the success or failure of many banks in the future. Successful development of digital and mobile banking will provide many opportunities for investment returns.

Where Might Banks Hunt for Opportunities in Digital, Mobile Space?

In this section, we’ll look at some of the emerging opportunities in digital and mobile banking:

Creating leadership in the Digital/Mobile Space

Efficient Scale and Growth

Digital/Mobile at the Center of Customer Relationship

We’ll explore how each of these can open up new ways for banks to serve their customers.

Opportunity 1: Leadership in the Digital and Mobile Space

Contrary to popular belief, banking is a very adaptable agile industry and well-run banks need to remain agile regardless of scale. The average age of a bank is 103 years. Banks don’t last without constantly changing and improving. We’re living in an age of disruptive technological change. Change is also an opportunity. Technology makes agility and improvement easier and faster. Those who are able to adapt to changing conditions and lead the evolution will prosper while slower-moving banks will face headwinds from increased competition. Smaller, less capable banks used to be prime acquisition targets for banks looking to grow their geographic footprint, but now with the increasingly prominent advent of digital banking, these same banks become targets for competition to gain market share from. In the same way that Netflix streaming disrupted Blockbuster DVDs, digital and mobile banking is a simplified way to engage directly with the customer. Competition in banks does not only come from M&A, it can drop in from the Cloud or Mobile phone.

Opportunity 2: Efficient Scale and Growth

Bank branches have physical limitations on where and how they operate. However, digital and mobile banking apps enable engagements beyond the branch. From a customer’s point of view, functionality can save a trip to the drive through, ordering and filling out deposit slips and checks, waiting in line; essentially digital/mobile puts the bank in their pocket. The development cost for banks to create these types of technologies is one that can deliver ongoing gains in customer engagement and stickiness. Therefore, when a digital and mobile banking strategy meshes with the bank’s overall goals, the bank can scale to reach customers wherever they are. Over time the bank should see benefits of a lower efficiency/higher profitability ratio as a result of the increased scale and efficiency.

Indirect benefits also come along with better quality digital banking. Banks that operate in multiple product spaces, digital and mobile are good methods to ensure that the bank can deliver the full experience to a customer such as additional services offered by the bank like brokerage, wealth management, etc., The lower churn/higher retention of these same clients comes along when the mobile bank is available.

Opportunity 3: Digital and Mobile at the center of customer relationships

Digital Banking shouldn’t be thought of as a bolt-on for traditional banking. While Digital and mobile banking have the ability to replace many forms of traditional banking and ease most regular banking tasks like money transfer, making deposits, checking balances, placing check holds etc.., having a strategy for building on the opportunities of the digital platform and connection can make or break a bank. Bank of America knows this and their strategy is worth examining. The bank offers many products for digital which not only make a lot of processes easier but also potentially create higher value customers. For example, once a customer is using their app or website they can offer them help with financial planning with product Life Plan or bring them into their Merrill Lynch universe with products like Merrill Guided Investing or Merrill Advisor Match. All of these services are opportunities to get more valuable customers than traditional banking equivalents due to digital automation and efficiency benefits.

A customer acquired for digital banking services potentially improves their retention and value if they continue to use the service in spite of moving geographically. Before digital, moving states meant moving banks. When I moved from Minnesota to Massachusetts, my bank did not have any branches in Massachusetts, but thanks to digital and mobile tech, I never had to change banks. In consumer banks, digital and mobile mean that professionals moving from job to job can remain with institutions and young people moving away from home can stay loyal to their first bank.

Digital banking isn’t just for the retail consumer. In commercial banking, businesses can scale their operations around the country and remain with the same institution. Commercial customers can grow with their bank instead of outgrowing them. Corporations benefit from digital products offered by banks. CashPro, a digital service offered by Bank of America enables corporations to pay and move large amounts of money with ease. Small businesses and even large enterprises that don’t have their own internal technology teams will take advantage of the digital offerings created by banks. There is potential for commercial digital product offerings to grow as more banking interactions are automated or simplified.

What New Threats Should Banks Watch for in the Digital/Mobile Space?

Banks need to face digital and mobile threats head-on. They need to beat out other competitors to control the space because it is crucial to future commerce and global operations. If they do not become a more dominant part of the space they will be left to do the heavy lifting without the rewards. Digital wallets are already in action through ApplePay and AndroidPay. The threat to banks' market share is ever present, but banks can’t compete on every front. In order to stay in the game, banks need to be on their front feet because digital and mobile competitors are not in the future - they are here now.

The potential opportunities from digital/mobile banking are inseparable from the downside threats of new competition in the flat, digital world. We’ll dive into these challenges below:

Managing Risks

Blending Culture

Evolution or Extinction

Each of these threats results not so much from the technology itself, as from the new array of competition that technology opens up.

Threat 1: Managing Risks

Moving to digital and mobile is not as simple as “building the system and they will come” or “buy a bank with an app and they will come”. Study M&T Bank’s 2022 annual report to see where they talked about difficulties in converting clients to their systems from acquisitions and where they illustrate the difficulties in fully grasping the potential:

“Our system conversion issues largely centered around online access and capabilities. The People’s United merger was the first one for M&T where online and mobile banking featured prominently. While it’s true that those capabilities existed when we merged with Hudson City in 2015 and Wilmington Trust in 2011, they weren’t woven into the fabric of everyday life to the extent they are today. That notwithstanding, we ambitiously set out to “convert” our new consumer and commercial customers to the M&T systems in such a way that they wouldn’t even notice the change. For many that was the case, for others, not so much. In banking, there is no “A” for effort.“

M&T 2022 Annual Report

This is not to disparage M&T’s efforts, in fact, it’s quite the opposite. Where many in the industry use annual reports as success theater, it is very valuable when those, like M&T leaders, recognize areas for improvement. While the potential for scale and growth in technological change is immense in banking, failures are common in tech projects; they are also expensive.

Threat 2: Blending Cultures

Many banks have cracked the code on creating strong banking cultures, but most don’t translate to our social culture. Banks have yet to embrace tech culture. The user experience is a big deal to consumers. If banks discount the user experience, tech players will pass them. For example, Venmo and Zelle offer the same service. They both transfer money. From the backend, Zelle is better. With Zelle, the money transfers directly into your account. Zelle uses a phone number that is searchable in your own contacts (much more efficient and secure) while Venmo uses social media type names that are harder to verify and Venmo adds an inconvenient step by putting your money in a Venmo account. Yet Venmo has a much higher saturation of use over Zelle. Zelle is utilitarian while Venmo appeals to young people who have been brought up on mobile phones and social media instead of filling out deposit slips and getting cash at an ATM. Venmo is built by tech people, is fun and engaging. It’s social. The platform is set up the same way as Instagram and focuses on the user experience platform, not just functionality. This example shows how banks need to embrace the user experience and culture to be relevant.

Culture is crucial to understanding consumer needs and to creating the right product to meet those needs. Most banks have not created the culture within their technology teams to do this. Extracting the value from new technologies requires people who understand the problem that banks are trying to solve for their customers with the people who can build and deliver great customer experiences. These skills are not a check-the-box exercise. Just having a financial tech team isn’t good enough. You must have people focused on driving the user experience solution for the customer.

Digital and mobile banking present a lot of challenges. There are many difficult steps before a bank can fully realize the potential benefits. Building a high-quality technology team with the right understanding of the problems and the culture to attack those problems is difficult. Finding the best way to mesh financial and technological capabilities adds uncertainty. Even after creating a successful system, it takes diligence to keep it on or near the cutting edge.

The users of digital banking apps, websites, and overall systems are the arbiters of their success. Their ease and popularity will determine their ability to prosper against the competition and potentially help small banks outpace larger ones, just like traditional banking digital banking is about people - the customers and the technologists.

Threat 3: Evolution or Extinction

I see three areas where banks need to strategize for success in the digital age.

First, banks need to be able to compete against banks in similar sizes and geographies. On one hand, this is the same as it ever was, but digital and mobile open up new threats. Similarly sized and situated banks often rely on the same outsourced players to build and operate tech which makes it harder to differentiate services.

Next, is the threat from the big four banks. The winner-take-all dynamic in networked technologies creates massive pressure on the thousands of smaller banks in the US. The biggest four banks can build their own tech teams from scratch and are not beholden to the limited menu of options available from outsourced players used by most of the other banks. The largest banks can invest in tech at a level that smaller rivals cannot. Large banks are investing huge amounts of money into digital development. Over the past 3 years, technology has accounted for approximately half of all investment into new opportunities by JP Morgan Chase. Last year alone the company spent $7.2b in technology investments. This is more than the assets under management of most banks in the US and the bank has been growing these tech investments at about 7% per year. This spend translates into scale - JP Morgan reported over 63m active digital users in 2023 and Bank of America reported 56m digital users in 2022. The scale at which these companies are operating is similar to that of streaming services or other large online platforms.

The third threat to banks, big and small, is big technology companies like Apple, Google, and Amazon with their huge existing user networks and go-to-market knowledge in the digital space. ApplePay brought in $782m in revenue for Apple in 2022 (which is double 2020). ApplePay is also activated on 78% of iPhones in the US. AndroidPay, while not as well networked or scaled, is still a significant player. These companies are increasing their financial service offerings and building some pieces of the digital financial infrastructure that banks haven’t been able to figure out yet.

Additionally, digital banking compounds the threat by adding new engagement combinations all the way through to merchant systems. For example, Amazon has begun to implement hand print scanning at some Whole Foods locations. This combination of their payments system, their online presence, and a large grocery store chain means some consumers can consolidate practically all expenses to the Amazon payments network. Banks need to meaningfully improve just to catch up. If banks were left on their own to create technological financial solutions they would eventually create quality systems. But, tech companies have already figured out a portion of the process that was not originally in the banker’s wheelhouse. Problem-solving and building must happen faster, and better. Battle lines are being drawn, and banks and tech players are figuring out where they will play most effectively. Dave Birch, Director at Consult Hyperion, cautions banks that “The leather wallet is yours, the digital wallet is not.”

How Should Banks Navigate these Challenges?

Faced with both opportunities and threats in digital/mobile, how should banks find a way through? There is no single playbook that governs all digital/ mobile bank strategies, but there are underlying capabilities that banks can build on. Overall, banks need to find the match of their internal strengths where they meet the external threats and opportunities we have discussed. For example, how should bankers think about competing with behemoths in both the financial space and the technology space? One answer may be from Aditya Puri, who built HDFC Bank in India, when asked about the competition from fintech players he replied that it was like making chicken curry, the new players have all the spices to make the curry, but he has the chicken. Staying as close as possible to the customer (chicken) is one advantage banks can maximize further with the features from digital/mobile technologies.

We’ll look at three ways to pursue digital/ mobile while learning quickly to avoid inevitable downside threats:

Developing Digital/Mobile Strength

Learning with Analytics

Capital Allocation

Challenge 1: Develop Digital and Mobile Strength

Currently, digital banking does not encompass the full array of services available in a physical branch.FirstBank is a great example of how to leverage digital/mobile tech to focus on prioritizing their customer's needs by building a better user experience. FirstBank prides itself on being technology-forward, however, it doesn’t have the size or budget for R&D at the scale of the largest banks or large technology companies being first to market with features like voice assistance or AI financial services. For example, there is nothing more basic to using an app than logging in with passwords. Focusing here helped FirstBank find something stronger and simpler than passwords. They built a process to enter the FirstBank app efficiently with biometric login (Face ID).

FirstBank services offerings include Mobile Deposit, Zelle, Bill Pay, Digital Wallet, Card Management, Biometric Login, and a Communication Center. Their customers want to be able to move money and redirect it without talking to a customer service representative or going into a branch. Customers can do most regular tasks right in the app like cashing checks, transferring money, paying bills, using digital payment systems, and more. In the case there are problems or questions FirstBank still offers customer support to help.

Banks have different customers with different needs. Digital banking will need to reflect this. For example, one bank may be looking to scale without increasing its branch count. This means they may want easy ways to deposit checks, consult bank employees virtually, and more. Other banks may be more focused on helping commercial clients by giving them online or in-app resources for day-to-day tasks. Some banks like Triumph may be using technology to build fundamentally new payment systems. Smaller banks may have their best shot at capitalizing on digital by organizing their offering first on the core wants and needs of their customers and then growing from there.

Challenge 2: Learning with Analytics

While customer-facing features get the bulk of attention, real traction may be found in the back-end tech with analytics. What customers are looking for is often capability and simplicity, but how should banks measure their success rate here? Growth in customers, retention, loans, and deposits are factors that tell a big-picture story. But more detail can help show areas that are worth highlighting- what is the cycle time to open up a new customer account? How many interactions are a hybrid digital and physical interactions or involve higher value customers? And which interactions create higher value engagement such as connecting to relationship managers?

To return to fundamentals - a key part of the Banking Flywheel is lowering loan losses. This is done by getting higher quality customers, but even with very strict criteria for who qualifies for loans, there will still be some customers who slip through the cracks. Conversely, there will be customers who get denied who will pay back the loan. Banks use data on customers from credit scores, collateral, lending history, and more to make loan decisions. Digital banking gives more opportunities to better understand the customers. If digital banking allows for longer retention of a customer, the picture of the customer’s viability comes into clearer focus. Banks will be able to see if customers use financial goal-setting features and if they hit those goals early or at all. These can become key drivers in the decision-making process for loaning that haven’t previously been accessible.

And finally, using analytics means that banks can learn quickly. Data will reveal what features work for consumers, what products are being used, and where they are gaining or losing engagement. Banks can quickly tailor their resources to develop products after learning from prototypes and how new deployments fare in real-world use.

Challenge 3: Capital Allocation

Bankers need to think beyond maps. They need to think about demographics and capabilities. In theory, digital/mobile banking can simulate the type of expansion growth that was previously available to strategies like serial acquirers. Much of the cost for continuous acquisition growth is now converted to the expense of a digital and integration tech team.

However, tech development is capital-intensive and requires capital allocators with a good handle on both challenges and opportunities, plus a tangible plan. A digital strategy can’t be outsourced even if the development can. The cost of wasted efforts in tech is significant. Digital strategy can seem great in theory, but the intelligent capital allocator needs to stay close to the implementation and results and make sure to look beyond the PowerPoint presentation. The process is attention intensive by management, difficult, and expensive whether it works or not. Expensive to win; and even more expensive to lose.

Conclusion

Digital banking is the key to the next era of banking. Maxfield’s Flywheel shows a framework where traditional banks can grow significantly with a few small improvements working together and point to efficiency as a key element to set the flywheel in motion. The potential efficiency arising from the adoption of digital interfaces seems obvious, but in order to achieve the benefits there are some major challenges and threats to overcome. The new opportunities also mean new players from big tech and new strategies could be lethal to some banks. The entire landscape is changing now; it is time for banks to evolve and adapt. If they do they will be able to serve their customers better, operate efficiently, become more profitable, and scale beyond their physical footprint.

Footnote

For some brilliant insight and a deep dive into the virtuous cycle of banking read this:

“The Flywheel of Banking” by John Maxfield, https://www.bankdirector.com/wp-content/uploads/nCino-Report-The-Flywheel-of-Banking.pdf

Digital banking provides a lot of opportunities for investment returns. To learn more of how I analyze the digital side of a bank from an investor's perspective stay tuned for part two.