CAVA Shouldn't Be A Value Stock (Issue #71)

CAVA Shouldn't Be A Value Stock (Issue #71)

Investment Thesis

CAVA is a stock that will be added to my watchlist because while I’m not sure it will be quite as exciting as Chipotle 20 years ago it still seems like a strong growth opportunity. The currently high valuation and low margins make it a more difficult investment to justify. However, the demand and potential for expansion as well as the execution of expansion seems to be working well. I will be curious to see how they can become profitable and move from a growth model to a more sustainable long-term model as the company gets to scale.

Company Overview

CAVA the Mediterranean fast casual eatery IPOed a month ago and has often been called “the next Chipotle.” While I’m not sure this is the case let’s jump into understanding if it could still be a good opportunity.

In 2018, CAVA acquired Zoe’s Kitchen, a Mediterranean chain with 260 locations, for $300m. This is important because it takes the company 4-5 weeks from breaking ground to opening a CAVA when converting from a Zoe’s compared to 14-16 weeks to build a CAVA from scratch. At that same time, CAVA only had ~70 locations and is now on track to finish the year with 302 locations (almost triple the count in 2020). At the end of that same year Founder and former CEO of Panera became Chairman of CAVA.

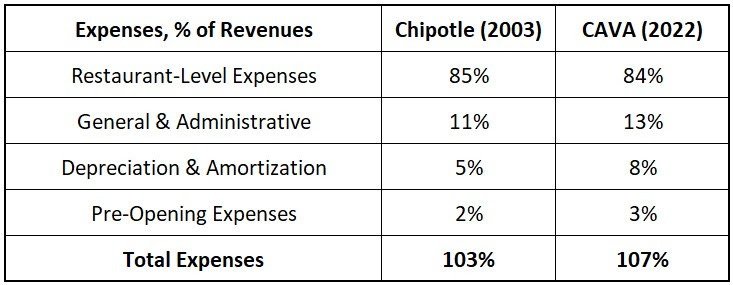

Chipotle 2003 —> Alex TSOH

“While Chipotle attracted a few skeptics 17 years ago, its market value after its initial surge was just $1.43 billion; it was profitable and had more than 450 restaurants. Cava has 263 restaurants, isn’t yet profitable and had a market value of $5.4 billion at Friday’s close.”

Alex Morris, who writes TSOH Investment Research, did a great deep dive on CAVA, comparing it to Chipotle in 2003. There are many parallels to be made when it comes to scale, size, and store count. However, some key differences can be noticed as well. For example, while Restaurant LEvel Expenses are comparable Restaurant Level EBIT Margins for Chipotle 2003 were ~15% compared to ~20% for CAVA 2022 and ~25% for CAVA Q1 2023. On the other hand, what CAVA lacks compared to Chipotle 2003 is Below-The-Line Expenses (any non-Restaurant Level Expenses including start-up costs). Chipotle 2003 Below-The-Line expenses were ~18% compared to CAVA 2022 ~24%. If you want more Chipotle 2003 and CAVA 2022 comparisons check it out at TSOH LINK.

Source:

For a unit volume comparison, CAVA produces $2.5m in unit volume versus Chipotle at currently $2.8m (leading the category). Also, the average CAVA location has 400 fewer square feet than the average Chipotle making CAVA more unit volume per square foot. This bodes well for the bull case showing that CAVA already has significant popularity among consumers where it currently resides. Looking forward, it will be interesting to see how this grows or changes and if it is harmed/diluted by more location density within cities.

ShakeShack

Another example of a successful comparison is ShakeShack. The chain has 449 locations that produced ~$253m in revenue and ~$395m in system-wide sales in Q1 2023. While this is about half the revenue of CAVA in the same period and ShakeShack has ~60% more locations the company (ShakeShack) was able to make $28m in Adjusted EBITDA. Meaning ShakeShack has less unit volume or revenue per location, but better system efficiency to make a profit from less revenue.

Sweetgreen

Most restaurants and chains don't succeed. The restaurant business is very risky and extremely difficult with low margins, high overhead, and seemingly infinite variables. Further, even those that survive don’t always prosper. A prime example of this is Sweetgreen, while they made be a trendy chain their stock has tanked from ~$50 to ~$15 per share today since their late 2021 IPO. Their macro timing was not conducive to a successful start to their public offering there is more negative to the story.

CAVA produced 4x more revenue in Q1 2023 than Sweetgreen’s $125m while CAVA only has ~17% more locations. In 2022, Sweetgreen had a 15% Restaurant Level Margin compared to 16% from CAVA.

Looking Forward

With the projection of ~1000 stores or a little less than 4x by 2032 CAVA with have to both grow its margins as well as scale to go from an interesting or extremely exciting stock.

Valuation

CAVA is pretty expensive almost any way you look at it. Now I am all for paying for quality and if you quantify quality as revenue per store and total revenue then CAVA is extremely valuable. That said earnings are still non-existent for two reasons. First, the start-up costs of opening new locations are significant. Second, the operations margins are small. As the company gets to scale (and is opening fewer locations) then it will be profitable.

CAVA is far from a value stock, but that might be a good thing. As we know a successful investment can only be created by having other people (individuals, funds, etc.) agree with your positive outlook on a company. CAVA is at a high, but not an astronomical valuation. This shows confidence on the part of investors for the company’s future. As we move forward if CAVA is able to expand to its 1000 locations by 2032 and become more efficient as start-up costs drop then there is a lot of promise for the stock. This all ties into Michael Mauboussin’s idea of Expectations Investing.

While all of this is important CAVA still trades at 8.3x Price/Sales. This might be cheap for a growth business it is still expensive for a culinary business (a high-risk industry).

Until Sunday,

Soren

Thanks for the shout out Soren!