Boston Omaha: Evolving Capital Allocators

Now the dust has settled and it is time to see if the updated management team led by Adam Peterson

This is not a deep dive on Boston Omaha (NYSE: BOC — $458.37mm), I linked my slightly outdated deep dive on it to familiarize those not already versed in the business. The company trades at a third of its 2021 highs, but is this justified? In the past year alone it has experienced significant hits to its reputation due to a lack of clear information from management during the exit of co-CEO and co-builder of the business Alex Rozek. Now the dust has settled and it is time to see if the updated management team led by Adam Peterson, the other co-CEO and builder of the business, is on the right track.

After Rozek’s exit management’s message was clear: the company is focused on building existing ventures and improving the efficiency of business units. New ventures are not the near-term focus.

To start let’s break down the situation piece by piece.

Link Media:

The wholly owned subsidiary and 6th largest US billboard company (7,600 faces) produced $33mm in revenue and $5.1mm net income YTD as of last reporting. This segment has seen recent tailwinds from lowering land costs through easement purchases and renewed land leases. This unit is not a growth engine; instead, it plays the role of a cash cow as it increases efficiency.

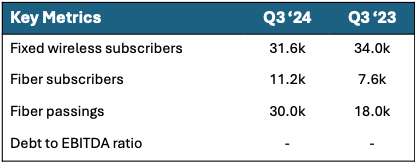

Boston Omaha Broadband (BOB):

Broadband is probably the most complex piece of the business represented by 4 different fiber/broadband businesses: AireBeam, InfoWest, Utah Broadband, and Fiber Fast Homes. It is separated for most reporting into two segments the separate brands; AireBeam, InfoWest, and Utah Broadband; and the special unit; Fiber Fast Homes (FFH). The former is operating a hair below breakeven (net loss $200k) with a significant gross margin of 79.2%, but large investment expenditures keeping profitability just out of reach. FFH a much smaller business at $1mm in revenue does not have the same efficiency with a -52.7% gross margin.

AireBeam, InfoWest, and Utah Broadband Combined

Fiber Fast Homes

Not all capital invested is seeing cash flow yet; however, that is not an indicator of future revenue. As communities develop, new patrons can subscribe to fiber at varying levels, meaning that with new homes being built there are still ways to increase revenues organically. Last spring, there was some reflective messaging about this particular business unit from management saying that not all of the capital invested in fixed wireless for new and existing customers was worth it.

General Indemnity Group (GIG):

The surety insurance company produced $19.2mm in gross written premium, $17.3mm in revenue, and $2.2mm in net income YTD as of the last reporting period. This translates to a 52.8% year/year increase in gross written premium. On the income statement, revenues grew by 32.4% year/year while net income grew by 96.8%. Management appears to view this as an attractive area for reinvestment with increasing efficiency, as opposed to the 2021 view that this was an example of a place where capital would get “stuck.” I speculate that this new vigor in the insurance business is an example of the difference in thinking between previous and current management. GIG will continue to be a key part of the business to track as the company grows and evolves.

SkyHarbour:

SkyHarbour (NYSE: SKYH — $816.51mm) a private aircraft hangar rental business that can be viewed similarly to a specialty REIT went public through a Boston Omaha-sponsored SPAC. Boston Omaha holds the company through Class A common stock with a market value of $134.7mm and warrants with a market value of $18.8mm. The warrants are not activated until the common shares surpass $11.50/share while they currently sit at $10.83.

Notes On Valuation:

I understand the general negativity associated with the Co-CEO and Co-Chairman exiting the company and taking a pound of flesh with him in the form of cash and SkyHarbour stock, but the company currently trades at 87% of book value. I’m not convinced that is a justified discount.

The billboard business at a conservative 20x earnings multiple has an ~$140mm valuation. This does not include any valuation premiums for the inherent moats that the billboard industry provides. Management has said previously that they wouldn’t sell the business for $300mm which brings confidence that this business possesses more attractive long-term potential than what meets the surface.

Back in 2021 at their annual meeting management gave an estimated value per subscriber of ~$3k. This is in line with the amounts paid by Boston Omaha in acquisitions in the sector. This would value the combined fiber/broadband business at $136.8mm.

Investments mainly comprised of SKYH stock and warrants have a GAAP value of $123.5mm, but that marks down the SKYH combined holding to $90.2mm from the current market value of $153.5mm, it is an underestimate of true value, to say the least. Following the GAAP value and adjusting the SKYH holding for market value would put this branch of the business at a $186.8mm value.

Just putting these pieces together and adding cash would bring an estimated $492.7mm valuation. This excludes the insurance business, bank, and some other assets. The company currently trades at a $458.37mm market cap. That’s a discount.

Closing Thoughts:

Boston Omaha may have been overestimated at a few years ago, but there has been an overcorrection. The company is still positioned for strong long-term growth and the management team is more focused than ever. Efficiency within business units is a priority and we are already seeing results of this in the insurance and billboard branches. There are some unknowns in the broadband business, but at this valuation, there is room for error. I’m looking forward to seeing how they perform as the company evolves.

Additionally, I wanted to include some recent write-ups I’ve found particularly interesting:

— Berkshire Hathaway’s Culture in 2050Sets the stage for the just released BRK 2024 Annual Report and the next steps for management

Discusses pressures to split Class A shares

General lack of transparency to just a premium valuation

Using mobile games to promote online gambling

Potential fraud and other scandals

Focuses on the outperformance of companies that consistently buy back stock

Dillard’s, eBay, O’Reilly, and more

Until Sunday,

Soren